5 Steps to Create a Family Budget and End Money Fights

Let’s be honest. It’s the 28th of the month. You get that familiar, sinking feeling in your stomach. You check your bank account, and the number staring back is… smaller than you hoped. Way smaller. This is exactly why budget planning matters—and why you’re here looking for answers.

Now, the anxiety kicks in. You start making quiet, desperate little deals with yourself. “Okay, just cereal for dinner. No driving anywhere. Please, no one has an emergency.”

This isn’t living. It’s a low-grade financial panic that repeats every 30 days. You’ve probably tried to fix it. You downloaded an app, made a spreadsheet, or even bought envelopes. But after a week, it all fell apart.

Why? Because you were told budget planning is a math problem. It’s not.

It’s a behavior problem. It’s a communication problem. And most of all, it’s a problem with permission.

This is not another article that will tell you to stop buying lattes. This is a comprehensive guide to building a spending plan that works for your real, messy, wonderful human life. It’s a plan that gives you permission to spend, not just a system that punishes you for it.

What You Will Discover in This Guide

This is a 3,000-word deep dive designed to be the last budgeting guide you’ll ever need. We’re going beyond the basics and tackling the real-world friction points that cause 90% of budgets to fail.

- The Psychological Switch: Why you need to stop “budgeting” and start “freedom planning.” This one mindset shift changes the entire game.

- The Partner Problem: A step-by-step communication script for getting your spouse or partner on board—even if they hate talking about money.

- Real-World Case Studies: We’ll follow “Mark and Sarah” and show how they went from fighting about money to finding an extra $1,200 a month.

- The Right Method (For You): An honest breakdown of Zero-Based, 50/30/20, and hybrid methods, helping you choose based on your personality, not a guru’s dogma.

- Honest Tool Reviews: My no-nonsense take on 8+ budgeting tools (like YNAB, Monarch, and Tiller), what they cost, and who they’re really for. (Hot take: most are a waste of money).

- The Failure Protocol: A simple, 3-step process for what to do when you inevitably overspend (because you will, and that’s okay).

My goal is to give you back your control. Not just over your money, but over your time, your choices, and your future. Let’s build a plan that serves you, not the other way around.

Why Does Every Budget I Try Seem to Fail?

Here’s the short answer: Your budget failed because it was too rigid, it didn’t align with your values, or it treated you like a robot instead of a human. A budget isn’t a cage; it’s a blueprint. If the blueprint is flawed or doesn’t account for reality (like, you know, needing to buy a birthday present), the whole structure will collapse.

Here’s what nobody tells you about budget failure: it’s not a moral failing. It’s a data problem.

We set up budgets based on an “ideal” version of ourselves. The “ideal you” cooks every meal, never buys coffee, and finds joy in spreadsheets. The “real you” is tired, busy, and just wants a pizza on Friday. Your budget fails when the “ideal you” makes a plan that the “real you” can’t possibly follow.

The second reason is that we focus on restrictions, not permission. The word “budget” feels like a diet. It’s about what you can’t have. No wonder we rebel against it!

Confession Booth: My Big Budgeting Failure

I’m a personal finance writer, and I failed at budgeting for years. I was a “YNAB Classic” devotee (that’s You Need A Budget for the uninitiated). I tracked every single penny. I spent hours “reconciling” my accounts. And I was miserable.

One month, I forgot to track a $15 lunch. It cascaded. By the end of the week, my software was a sea of red “overspent” categories. I felt so defeated that I just… quit. I didn’t open the app for six months. I failed because I was so obsessed with tracking the past, I forgot to plan. My perfectionism was the enemy of my progress.

The lesson? A “perfect” budget that you abandon is useless. A “messy but consistent” budget is life changing. Your budget will fail. Expect it. The goal is not to never fail; the goal is to have a system for when you do. We’ll cover that in the “Failure Protocol” section.

What Is a “Freedom Plan” and Why Is It Better Than a “Budget”?

This is the most important mindset shift you can make. Stop calling it a budget. Start calling it a Freedom Plan or a Spending Plan.

This isn’t just a silly word game. It’s a complete psychological reframing.

- A Budget asks: “How can I restrict my spending?”

- A Freedom Plan asks: “What do I want my money to do for me?”

See the difference? One is about chains; the other is about purpose. Your Freedom Plan gives every single dollar a job. That job might be “Pay Rent” (a boring but important job). It might be “Buy Groceries.” But it can also be “Guilt-Free Pizza Fund” or “Future Vacation to Italy.”

When you spend money from your “Guilt-Free Pizza Fund,” you don’t feel shame. You feel successful! You are executing the plan. You gave that money permission to be spent exactly that way.

This approach connects your daily spending (a $5 latte) to your big-picture goals (a $5,000 vacation). When you know that skipping the latte this time is actively funding your Italy trip, the choice becomes easier. It’s not deprivation; it’s a trade. You’re trading something you want now for something you want more.

How Do I Get My Partner on Board with Budgeting (Without Starting a Fight)?

Here’s what nobody tells you about family budgeting: It has almost nothing to do with money. It is a communication and values-alignment tool. The spreadsheet is the last 10% of the puzzle. The first 90% is getting on the same team.

Money fights are rarely about the dollars. They are about what the dollars represent: Security, Freedom, Trust, Respect, or Power.

When you say, “We need to stop spending so much on takeout,” your partner might hear, “You don’t respect the hard work I do, and you’re trying to control me.” It triggers a defensive-aggressive spiral.

Stop talking about spreadsheets. Start talking about dreams.

The “Dream Meeting” (No Spreadsheets Allowed)

Schedule a time. Call it a “State of the Union” or “Dream Meeting.” No laptops. No bank statements. Just you, your partner, a notebook, and maybe a glass of wine.

Step 1: Ask This One Question. “In a perfect world, five years from now, what does our life look like?” Let them dream. Don’t judge. Write it all down. Do you travel more? Do you work less? Do you own a home? Are your debt-free?

Step 2: Connect Dreams to Reality. Now, look at the list. “I love these goals. What’s one thing that’s stopping us from getting there?” The answer will, almost always, be money.

Step 3: Frame the Budget as the Tool. Now, you introduce the plan. “What if we created a plan for our money a Freedom Plan that was designed specifically to make [Dream Goal #1] happen? It wouldn’t be about restriction. It would be about telling our money to build that.”

You are no longer a critic. You are a co-conspirator. You’re on the same team, fighting for your dreams, not against each other.

Contrarian Opinion: Joint Accounts Aren’t Always the Answer

Every guru scream “Combine your finances!” For some, it works. For others, it’s a disaster. I’ve seen more success with a “Yours, Mine, and Ours” system.

- “Ours” (Joint Checking): All shared bills go here (mortgage/rent, utilities, groceries, kid’s expenses). You each contribute a set, proportional amount from your paychecks.

- “Yours” (Personal Account): This is your money. For you. To spend, save, or invest as you wish, 100% guilt-free.

- “Mine” (Personal Account): Same for your partner.

This system eliminates the “Are you really buying another pair of shoes?” fights. It builds trust and autonomy while ensuring all shared goals are met.

What Are the Very First Steps to Building a Budget from Scratch?

Your first step is not to make a budget. It’s to track your reality. You cannot make a realistic plan until you know where your money is going.

Most people skip this. They just guess. “I think we spend, like, $600 on groceries?” Then they discover it’s $1,100, and their entire plan blows up on day three.

Don’t guess. Know.

The “Zero-Judgment” 30-Day Audit:

For the next 30 days (or just the last 30, using your bank/credit card statements), you are an archaeologist. Your only job is to dig up the data and categorize every single dollar that left your life.

Use a simple notebook, a spreadsheet, or an app. The categories are:

- Fixed Needs: (Rent/Mortgage, Utilities, Car Payment, Insurance, Debt Payments)

- Variable Needs: (Groceries, Gas/Transport, Household Supplies, Kids’ Schooling)

- Wants: (Restaurants, Subscriptions, Hobbies, Shopping, Coffee)

- Savings/Goals: (Debt Overpayment, Investments, “Where did it go?!”)

At the end of 30 days, you will have your truth. It might be ugly. You might be horrified to see you spent $450 on DoorDash. This is not a time for shame. This is a time for celebration! You now have the data. You have found the leak. You can’t fix a leak you don’t know exists.

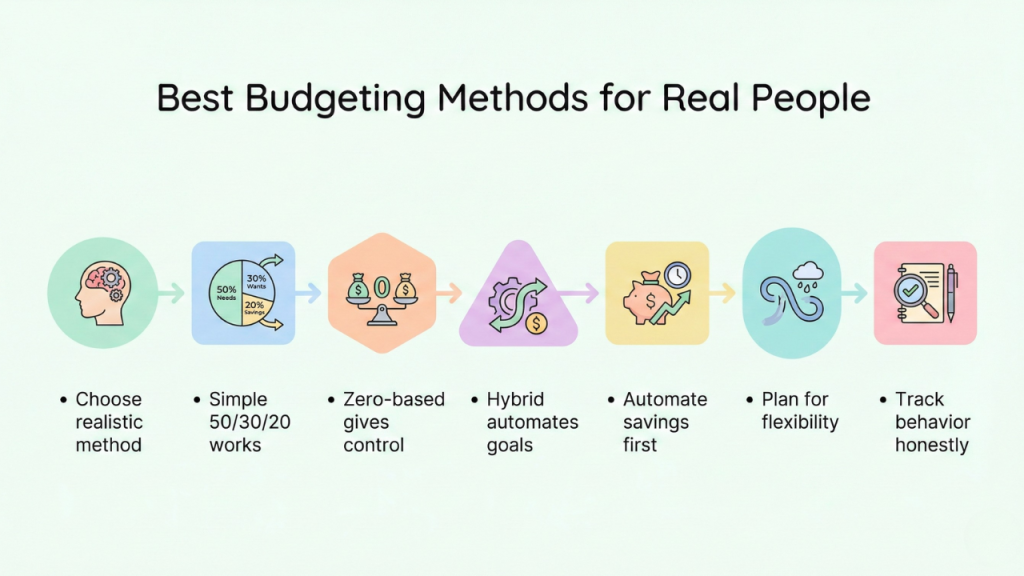

What Are the Best Budgeting Methods for Real People (Not Robots)?

Now that you have your data, you can choose a system to build your plan. Here’s the truth: the best budget planning method is the one you will stick with.

Here are the “Big 3,” explained for humans.

1. The 50/30/20 Rule (The “Good Enough” Budget)

- What it is: A simple framework, not a line-item budget. You divide your after-tax income into three buckets.

- 50% for Needs: (Rent, groceries, utilities, transport, insurance).

- 30% for Wants: (Restaurants, hobbies, shopping, Netflix).

- 20% for Savings/Debt: (Emergency fund, debt payoff, investments).

- Pros: Incredibly simple. Easy to maintain. Great for beginners who feel overwhelmed. It prevents “death by a thousand spreadsheets.”

- Cons: The percentages might be totally unrealistic for you. If you’re in a high cost-of-living area, your “Needs” might be 70%. It doesn’t help you optimize spending.

- Best for: Beginners, people who hate details, and those with stable incomes.

2. The Zero-Based Budget (The “High-Control” Budget)

- What it is: This is the method I personally use, and it’s the engine behind tools like YNAB. It’s not as scary as it sounds. It just means Income – Expenses = Zero.

- You give every single dollar a job before the month begins. If you make $5,000, you assign all $5,000 to categories (including savings and debt).

- Pros: You have total control. You know where every dollar is going. It’s the fastest way to change your financial picture, pay off debt, and save aggressively.

- Cons: It’s time-consuming. It requires you to be engaged (at least weekly). It can feel restrictive if you don’t build in “Fun Money” categories.

- Best for: People who love a plan, “Type A” personalities, those with irregular income (we’ll cover this), and anyone on a mission to destroy debt.

3. The “Hybrid” or “Pay Yourself First” Method (My Personal Favorite)

- What it is: A mix of the two. It front-loads your most important goals.

- How it works: The moment you get paid, you automate your goals.

- Day 1: Paycheck hits.

- Day 2: Automatic transfers go out:

- $X to your “Ours” joint account for bills.

- $Y to your high-yield savings (for emergency fund/sinking funds).

- $Z to your investment account.

- What’s left over is yours to manage. You can use a lost 50/30/20-style plan for the rest, knowing all your important goals have already been met. You’ve eaten your vegetables first.

- Pros: It’s automated, so it beats procrastination. It guarantees you will hit your savings goals. It offers freedom and flexibility after your priorities are funded.

- Cons: You need to be disciplined enough to make the rest of your money last.

- Best for: People who want to “set it and forget it,” procrastinators, and those who want to build wealth without tracking every penny.

How Do “Sinking Funds” Stop Budgets from Breaking?

This is the secret weapon. This is the one tactic that takes you from a “budget rookie” to a “budget master.”

A sinking fund is a mini savings account for a specific, known, non-monthly expense.

Why did your past budgets fail? Because Christmas happened. Or your car needed new tires. Or your kid had a birthday. These “surprises” aren’t surprises at all. They are predictable, but irregular, expenses.

You don’t budget for $1,200 on new tires in October. You budget $100 a month all year for “Car Maintenance.”

You don’t budget $600 for holiday gifts in December. You budget $50 a month all year for “Holidays.”

How to set them up:

- List all your major non-monthly expenses: Holidays, Birthdays, Car Maintenance, Home Repair, Annual Subscriptions, Vacation.

- Estimate the total annual cost (e.g., Holidays = $600).

- Divide by 12 (e.g., $600 / 12 = $50).

- Create this as a category in your budget. You are “sinking” $50 into this fund every month.

You can keep this money in a separate high-yield savings account. When the expense arrives, you use that saved money. It’s not an emergency. It’s a plan. Your regular monthly budget (groceries, gas) is completely unharmed. This is the single biggest stress-reducer in all personal finances.

How Should I Budget If My Income Is Irregular?

This is the hard mode of budgeting. If you’re a freelancer, salesperson, or small business owner, the 50/30/20 rule is useless. The Zero-Based Budget is your new best friend.

Your entire approach should be backward. You don’t budget based on forecasted income. Your budget is based on cash on hand.

Step 1: Find Your “Baseline.” What is the absolute minimum you need to survive? (Rent, utilities, basic food). This is your “Bare Bones” number. Let’s say it’s $3,000.

Step 2: Create a “Buffer.” Your first goal is to save one full month of “Bare Bones” expenses ($3,000). This is your buffer. You keep it in your checking account.

Step 3: Live on Last Month’s Income. This is the magic trick. All the money you earn in November, you don’t touch. You put it aside. On December 1st, you use the total money you earned in November to fund your entire December budget.

You are now one month ahead. You’re no longer on the feast-or-famine roller coaster. You know exactly how much money you should work for the month. On a great month ($8,000), you fund everything and send a huge chunk to savings. On a bad month ($3,500), you can still cover your “Bare Bones” and just cut back on “Wants.” This system provides stability during chaos.

What Are the Best Budgeting Tools That Are Actually Worth Using?

This is the part of the article where most blogs just list 15 apps. I’m not going to do that. Here’s a controversial take: Most budgeting apps are a well-designed distraction. They make you feel productive for $15/month while you avoid the real work: deciding what’s important to you.

The tool does not matter. The behavior matters. A motivated person with a spiral notebook will beat a lazy person with the world’s best software, every single time.

That said, the right tool can reduce friction.

The 80/20 Tool Comparison (Honest Pros and Cons)

| Tool | Price | Best For | My Honest Take |

| A Simple Spreadsheet | Free | DIY-ers, Data Nerds | 10/10. It’s free, flexible, and forces you to be mindful. Use a free template from Tiller or build your own. This is what I use. |

| YNAB (You Need A Budget) | ~$14.99/mo | Zero-Based Budgeters, People on a Mission | YNAB is not a tracking app; it’s a methodology. It has a 3-day learning “cliff,” not a curve. If you commit, it will change your life. If you don’t, you’ll hate it. |

| Monarch Money | ~$14.99/mo | Ex-Mint Users, Net Worth Trackers | This is the new king now that Mint is gone. It’s a fantastic dashboard for all your accounts. It’s less a “budgeting” app and more a “financial overview” app. It’s expensive but powerful. |

| Tiller Money | ~$6.59/mo | Spreadsheet Lovers Who Hate Data Entry | Tiller is the magic bridge. It automatically pulls all your transactions into your own Google Sheet or Excel file. You get the automation of an app with the control of a spreadsheet. Brilliant. |

| Empower (fka Personal Capital) | Free | Investors, Net Worth Watchers | Their budgeting tools are “meh.” But their investment and retirement tracking are the best in the business, and it’s free. Use it to track your big picture, not your daily coffee. |

| EveryDollar (Ramsey) | Free (Basic) / $79.99/yr (Premium) | Ramsey Followers, Debt Haters | A very good, simple zero-based budgeting app. If you follow the “Baby Steps,” this is built for you. The free version (manual entry) is great. |

| Goodbudget | Free (Basic) / $8/mo | The “Envelope System” Crowd | A modern take on the cash envelope system. You create digital “envelopes” for your categories. Great for visual, tactile people. |

| Your Bank’s Free Tools | Free | Total Beginners | Before you pay for anything, check what your bank or credit card offers. Their free bucketing and tracking tools might be all you need. |

How Much Should I Really Be Budgeting for Groceries and “Fun”?

There is no magic number. Anyone who gives you one is lying. The USDA publishes a “Cost of Food” report, but it’s not very helpful for real-world planning.

Here is the only way to find your number:

- Use Your 30-Day Audit: What did you spend? Let’s say it was $1,100.

- Set a Realistic Goal: You are not going to $600 next month. That’s a recipe for failure. Try a 10% reduction. Your new goal is $990.

- Get Tactical: How will you hit $990? Not by “trying harder.” By having a plan. “I will meal plan on Sundays. I will only eat out once a week. I will check.”

- Track and Adjust: Did you hit $990? Great! Try $950 next month. Did you spend $1,050? That’s still a win! You’re $50 better. What went wrong? Adjust and try again.

For “Fun Money” (restaurants, hobbies, etc.), this is where your Values-Based Budgeting comes in. Look at your 30-Day Audit. Did you spend $400 on things that brought you real joy? Or was it $400 of mindless taps and subscriptions you forgot?

Assign a “Fun Money” number you and your partner agree on. Put it in a separate account or an envelope. When it’s gone, it’s gone. This is not restriction; it’s intentionality.

What Do I Do When I Inevitably Overspend?

Welcome to the club. This happens. It’s not a failure; it’s just a math problem to solve.

Do not light the whole budget on fire. Do not quit. You have a “Failure Protocol.”

When you overspend in a category (e.g., “Restaurants”), you have three and only three choices. This is called “Rolling with the Punches.”

- Cover It from Another “Want” Category: “Okay, I went $50 over on restaurants. I’ll move $50 from my ‘Shopping’ category to cover it. No shopping for me.” This is the best option.

- Cover It from a “Future” Category: I should cover this $50. I’ll take it from my ‘Vacation’ sinking fund and pay it back next month. This is less ideal but acceptable.

- Acknowledge It and Move On: “I went $50 over. It’s done. I can’t cover it. My savings will be $50 less this month. I will start fresh tomorrow.” This is the ‘nuclear option,’ but it’s still better than quitting.

The act of making the choice is what matters. You are still in control. You are acknowledging the overspend and giving that money a new job, even if that job is “covering a mistake.”

How Often Should I Review My Budget?

This depends on your method, but the answer is more often than you think.

- If you’re new or on a Zero-Based Budget: Once a week. (15 minutes). Have a “Money Date” with yourself or your partner. Reconcile transactions. Check your category balances. See what’s coming up for the week. This 15-minute check-in prevents 99% of all budget-breaking “surprises.”

- If you’re on a 50/30/20 or “Pay Yourself First” plan: Twice a month. Once at mid-month to see how your “Wants” and “Variable Needs” are tracking, and once at the end to make sure your automated savings went through.

- Everyone: Once a month. (30 minutes). This is your “look back and plan forward” meeting. How did you do last month? What’s new this month? (e.g., “Oh, right, Timmy’s birthday is this month. Let’s make sure that sinking fund is ready.”)

How Can I Teach My Kids About Budgeting?

You don’t teach them. You show them. They learn more from watching you (or fighting with you) about money than they ever will from a lecture.

The best way is to give them control over their own money.

- Age 5-8 (The “Clear Jars” Phase): Give them a small allowance. Get three clear jars: SPEND, SAVE, GIVE. When they get their money, they physically divide it. They can spend their “Spend” money on whatever they want. The “Save” jar is for a bigger toy. “Give” is for charity. They are learning the core concepts.

- Age 9-13 (The “Sinking Fund” Phase): They want a $120 video game. Don’t just buy it. Tell them, “Okay, that’s a goal. Let’s plan.” If their allowance is $10/week, show them how to save $10/week from their “Save” jar. They are learning to delay gratification and plan for a large purchase.

- Age 14+ (The “Real World” Phase): Open a teen checking account with a debit card. Give them a monthly “allowance” that is meant to cover all their wants: clothes, fast food, movie tickets. When they blow it all in one weekend… let them. This is the best $0 lesson they will ever learn. They will be broken for three weeks, and they will never make that mistake again. It’s better they learn with $100 now than with a $100,000 salary later.

When Does My Budget Stop Being About ‘Surviving’ and Start ‘Building Wealth’?

This is the beautiful final stage of budget planning.

The shift happens when your “Pay Yourself First” transfers become automatic and meaningful. In the beginning, your budget is about control plugging leaks and surviving.

After a few months, it becomes about optimization cutting back on things you don’t value to fund your sinking funds and get out of debt.

Finally, it becomes about growth. Your debt is gone. Your 3–6-month emergency fund is full. Now, that “Debt Payoff” line in your budget gets a new name: “Investments.”

That $500 you used to send to your credit card. Now it goes into your retirement account or a brokerage account every single month, automatically. Your budget’s job is no longer just to manage scarcity. Its job is to systematically, automatically build your wealth. Your Freedom Plan has done its job. It has brought you your freedom.

Frequently Asked Questions (The Real Talk)

1. What’s a realistic amount of time for this to not feel awful?

Honestly? 90 days. It takes three full monthly cycles to build the habit, find the leaks, and get a realistic plan. The first month is a mess. The second month is better. By the end of the third, you’ll feel that sense of control. Stick with it for one full quarter.

2. I’m afraid to look. What if it’s worse than I imagine?

It probably is. And that’s okay. The fear and anxiety you feel now, living in the dark, is 100x worse than reality. Knowing the truth, even if it’s ugly, is the first step to fixing it. The moment you see the numbers, the power shifts from the problem to you.

3. What’s the one category people forget to budget for?

Easy: “Stuff I Forgot to Budget For.” I am not kidding. Build this into your budget. $50, $100, whatever. A buffer category. Because you will forget your friend’s baby shower or the school field trip. This category is your safety net.

4. Should I pay off debt or save for an emergency fund first?

This is a hot debate. My answer: Do both.

Start by saving a “baby” emergency fund of $1,000. Do this as fast as you can. This stops you from going into more debt when a small emergency hits. Once you have that $1,000, pivot all your intensity to paying off high-interest debt (like credit cards). Once the debt is gone, go back and finish building your full 3–6-month emergency fund.

5. How can I budget for fluctuating bills, like electricity?

Look at your last 12 months of bills. Add them all up (e.g., $2,400 for the year) and divide them into 12 ($200/month). Budget this average amount every single month. Some months you’ll be under, some months you’ll be over, but it will all be balanced out. This is called “level billing,” and it brings stability to your plan.

6. My partner just won’t do this. Now what?

You can’t force them. But you can control your own money. Go back to the “Yours, Mine, and Ours” system. Agree on the “Ours” (the shared bills) and how much you each contribute. What they do with their “Mine” money is their business. What you do with yours is save, invest, and build your freedom. Often, when one partner starts modeling this financial calm and success, the other partner eventually becomes curious and wants to be in.

7. I tried the envelope system with cash, and I just… hate carrying cash.

Me too. It’s 2026. Use a digital version. An app like Goodbudget is a direct digital envelope system. Or, my favorite, open multiple high-yield savings accounts and name them. “Emergency Fund.” “Italy Vacation.” “Car Repair.” It’s the same concept, just digital.

8. What’s the best first step I can take right now?

Not a spreadsheet. Not an app. Automate $50. Log into your paycheck portal or bank account, and set up an automatic, recurring transfer. Have $50 move from your checking to a savings account the day after you get paid. Name that savings account “Freedom.” Congratulations. You’re officially a saver. Now, let’s build the plan to grow that.

Your New Beginning

This is a lot of information. I know it can feel overwhelming. Don’t try to do it all today.

Your journey to financial control is not a sprint. It’s a series of small, intentional steps, repeated over time. You don’t have to be perfect. You just have to be present. You have to decide that you’re tired of that end-of-month panic, and you’re ready to trade it for a feeling of control.

Your budget is not a judgment. It’s a tool. It’s the blueprint you design for the life you want to build.

My question for you is: What is the one dream you wrote down in that “Dream Meeting” that you’re going to start funding first?

Let me know. You can do this.

Jason Lee blends real-world budgeting experience with creative savings strategies shaped by his background in community outreach and financial education. He specializes in building practical systems—like zero-based budgets, sinking funds, and spending trackers—that regular families can actually stick with month after month. At Dollar Pioneer, Jason focuses on user-friendly guides, printables, and templates that make smart money management more accessible, less intimidating, and easier to turn into a weekly habit.