7 Best Budgeting Tips for Couples to Find Harmony Now

Introduction: Beyond Spreadsheets—Why Money Conflict is the Deadliest Threat to Your Relationship

Financial stress is a near-universal experience, yet its impact on romantic partnerships is uniquely corrosive. For many couples, money discussions transition quickly from simple logistics into intense, emotional battles that erode trust and connection. Ignoring this reality and approaching budgeting purely as an accounting exercise is the most common failure point for couples attempting to manage their finances together.

The magnitude of the problem is substantial. Surveys reveal that almost a third of partnered adults (31 percent) report that money is a major source of conflict in their relationship. However, the issue extends far beyond mere frequency; the conflicts themselves are fundamentally different from arguments over, for example, chores or children. Scholarly research indicates that money-related conflicts are consistently more intense, more problematic, and significantly more likely to remain unresolved compared to other sources of marital disagreement.

The Unresolved Battle: The Psychological Toxicity of Financial Conflict

When partners fight about money, they are rarely arguing about the price of a coffee machine or a specific utility bill. They often argue about perceived control, trust, and fundamental lifestyle values. This is why traditional, restrictive budgeting the “Accountant Mentality” fails couples. When a budget involves tracking every micro-transaction and requires permission for small purchases, it creates a toxic “money police” dynamic that rapidly transforms the relationship into a parent-child structure, poisoning intimacy.

Empirical data underscores the profound negativity associated with these disputes. Conflicts centered on money are reported as lasting significantly longer than non-money conflicts; wives, in one study, reported money conflicts lasting an average of 30.59 minutes, compared to 15.31 minutes for non-money conflicts. Furthermore, these conflicts are more recurrent, meaning they cover problems that have been discussed previously, failing to achieve true resolution.

The evidence suggests that money disputes serve as a high-stakes emotional minefield. They elicit greater use of angry and depressive behaviors from both partners, and critically, they are less likely to end in resolution, with partners often agreeing simply to continue the discussion later. The chronic nature of these unresolved arguments where the underlying issues of trust and power are never truly settled makes money tensions a significant predictor of marital distress and dissolution.

The foundational shift required for lasting financial harmony is to move entirely away from the daily tracking and policing that generates friction. Instead, couples must adopt a system based on automation, a defined shared vision, and guaranteed individual autonomy. This approach structurally removes the emotional triggers, allowing money management to become invisible and functional rather than a source of continuous negotiation.

🔻 Tip 1: The Partnership Prime Aligning Your Financial DNA

A budget is not merely a mathematical exercise; it is a living document of a couple’s shared values and future goals. Before any technical setup begins, partners must achieve complete alignment by understanding both their collective and individual financial psychologies. This initial step is designed to build the confidence and communication necessary for coordination.

The Non-Negotiable Conversation: Goals, Debts, and Full Disclosure

The first essential action is to institute a rule of total financial transparency. This “Full Disclosure” rule mandates that each partner openly share all details regarding their assets, debts, income, and recurring expenses as early as appropriate in the relationship. Attempting to budget while keeping financial secrets, even seemingly small ones, will quickly erode the trust necessary to succeed.

With transparency established, the conversation must immediately pivot to the long-term, shared goals. Discussing individual goals first such as paying off student loans or starting a specific business can provide empathy and context. Subsequently, defining mutual, big-picture objectives, like establishing a secure retirement, purchasing a home, or paying down shared debt, creates a unified sense of purpose. Agreeing with these major goals provides a rallying point and helps the couple find consensus on the day-to-day financial practices they must adopt to reach those targets. For instance, agreeing on a house purchase timeline provides the motivation needed to consistently contribute to a joint savings account.

Identifying and Leveraging Your Money Personalities

Every individual possesses a distinct financial DNA shaped significantly by their upbringing and life experiences. Common money styles include the Spontaneous type, the Security type, the Planner, and the Status seeker. These differences are normal but require empathy and patience to manage effectively.

For example, a partner with a “Spontaneous” money personality often struggles with saving and may experience guilt over spending. Conversely, a partner characterized as a “Planner” may become overly restrictive or frugal. If the Planner attempts to enforce a manual, restrictive budget on the Spontaneous partner, it results in continuous conflict and emotional suffocation, creating the harmful parent-child dynamic observed in toxic financial relationships.

The effective financial system must structurally accommodate these differences. By pre-allocating a dedicated portion of funds for guilt-free spending (as detailed in Tip 3), the system recognizes the Spontaneous partner’s need for discretionary purchases while simultaneously ensuring that all joint goals are funded first. This strategic move transforms the partner’s differing style from a relationship liability into a predictable, budgeted variable, enhancing mutual understanding and reducing anxiety around money.

🔻 Tip 2: Build the Foundation—The Hybrid Account Structure

The decision of how much money is “ours” versus “mine” is perhaps the most crucial logistical decision a couple faces. Total merging of finances can lead to relationship strain and the perception that one partner is responsible for managing all the money. However, managing everything separately often sacrifices convenience and financial clarity. The optimal strategy balances convenience, security, and autonomy through a hybrid account model.

When to Combine, When to Separate: Joint vs. Individual Accounts

While total joint accounts simplify shared expenses like rent, utilities, and groceries offering clear visibility into combined spending this approach is not universally adopted. Data indicates that 57% of American couples maintain at least some separate accounts, and 23% manage their finances entirely independently.

A combined checking account is highly convenient for paying shared bills, but it can complicate discretionary spending, forcing partners to constantly justify smaller personal purchases, leading directly back to the “money police” problem. The goal, therefore, is to merge the funds required for shared life and shared goals, while maintaining distinct boundaries for personal spending.

The 3-Account Strategy for Ultimate Autonomy and Responsibility

The following structure forms the backbone of the friction-minimizing approach, ensuring that shared responsibilities are met automatically while preserving individual freedom:

- Joint Checking Account (The Operating Hub): This account receives the combined monthly income (or the appropriate proportional contribution) and serves as the operational center for the household. All shared fixed costs rent, mortgage, insurance, utilities, groceries, and minimum debt payments are paid automatically from this account.

- Joint Savings Account (The Goal Builder): This account is dedicated to shared future goals and financial protection. It must hold the critical emergency fund but can also be segmented into sub-savings accounts to track specific goals, such as a down payment fund, a vacation fund, or a shared major purchase account. This segmentation provides clarity (Clarity, one of the five principles of financial harmony) and creates shared excitement as progress towards goals is tracked.

- Individual Spending Accounts (The Guilt-Free Zones): Each partner maintains their own separate checking account. A predetermined, equal, or proportional amount of discretionary money is automatically deposited here every month. This money is non-negotiable and requires zero judgment or discussion from the partner, irrespective of how it is spent (whether on expensive hobbies, books, or dining out).

This three-account architecture functions as a relationship lubricant. By structurally separating shared responsibilities (security) from personal autonomy (freedom), it eliminates the need to negotiate every small purchase. This systemic design directly combats the relationship-poisoning behavior of micromanagement, allowing couples to build wealth without constantly scrutinizing each other’s financial behavior.

🔻 Tip 3: Master the Flow with the Conscious Spending Plan (CSP)

To execute the 3-Account Strategy effectively, couples should adopt a modern, high-impact financial methodology that replaces tedious tracking with strategic allocation. The Conscious Spending Plan (CSP), also known as the anti-budget, focuses on automating large allocations rather than monitoring micro-transactions.

Moving Beyond Restriction: How the CSP (Anti-Budget) Works

Traditional budgeting requires couples to forecast spending for dozens of categories and meticulously track every dollar against those limits. Study after study shows this tedious approach is unsustainable and often leads to stress and shame.

CSP offers liberation from this restriction. It requires calculating the couple’s total monthly take-home income (after taxes and deductions) and then dividing this income into just four major categories using strategic percentages. By assigning these percentages and automating their distribution, the couple decides where their money should go before they have a chance to spend it, removing the stress associated with daily financial oversight.

The 4-Bucket Allocation Model: A Strategic Percentage Guide

The following table provides the foundational percentages for the CSP, demonstrating the necessary balance between immediate needs, long-term wealth, shared goals, and individual enjoyment:

The Conscious Spending Plan (CSP) Allocation Guide

| Category | Standard Allocation | Purpose | Adjustments (HCOL/Debt) |

| Fixed Costs (Needs) | 50-60% | Rent, Utilities, Minimum Debt Payments, Insurance | Up to 70% in high-cost-of-living areas |

| Investments (Future Wealth) | 10% | Retirement (401k/IRA), Brokerage Accounts | Prioritized heavily for early career couples |

| Savings (Shared Goals) | 5-10% | Emergency Fund, Down Payments, Vacation Funds | Prioritize emergency fund first |

| Guilt-Free Spending (Wants) | 20-35% | Personal purchases, hobbies, dining out | Reduced to 15-20% when aggressively paying down debt |

Customizing the Plan: Adjustments for HCOL, Debt, and Early Career

The most effective element of the CSP is its flexibility. The percentages are not rigid dogma but a starting point that must adapt to external realities and life stages. Recognizing this adaptability reinforces the plan as a living partnership agreement, which fundamentally builds Confidence and Clarity within the relationship.

- High-Cost-of-Living (HCOL) Areas: In regions with exceptionally high expenses (especially housing), the Fixed Costs bucket may need to temporarily increase to 65–70% of the total take-home income. This necessitates a temporary reduction in the Investments or Guilt-Free Spending categories until either income increases or the cost-of-living decreases. This acknowledges external economic pressures, such as high tariffs or moderating wage growth impacting purchasing power, which require continuous financial attention.

- Aggressive Debt Reduction: Couples focused on eliminating high-interest debt quickly should treat debt repayment exceeding the minimum monthly payment as a savings goal. To accelerate this process, the Guilt-Free Spending buffer should be reduced temporarily to 15–20%, reallocating those funds toward principal payments.

- Early Career Couples: Young couples are advised to prioritize Investments heavily to maximize compound growth over decades. Even if income is currently moderate, maximizing employer matching contributions to retirement accounts is critical, ensuring the “Investments” bucket is fully funded first.

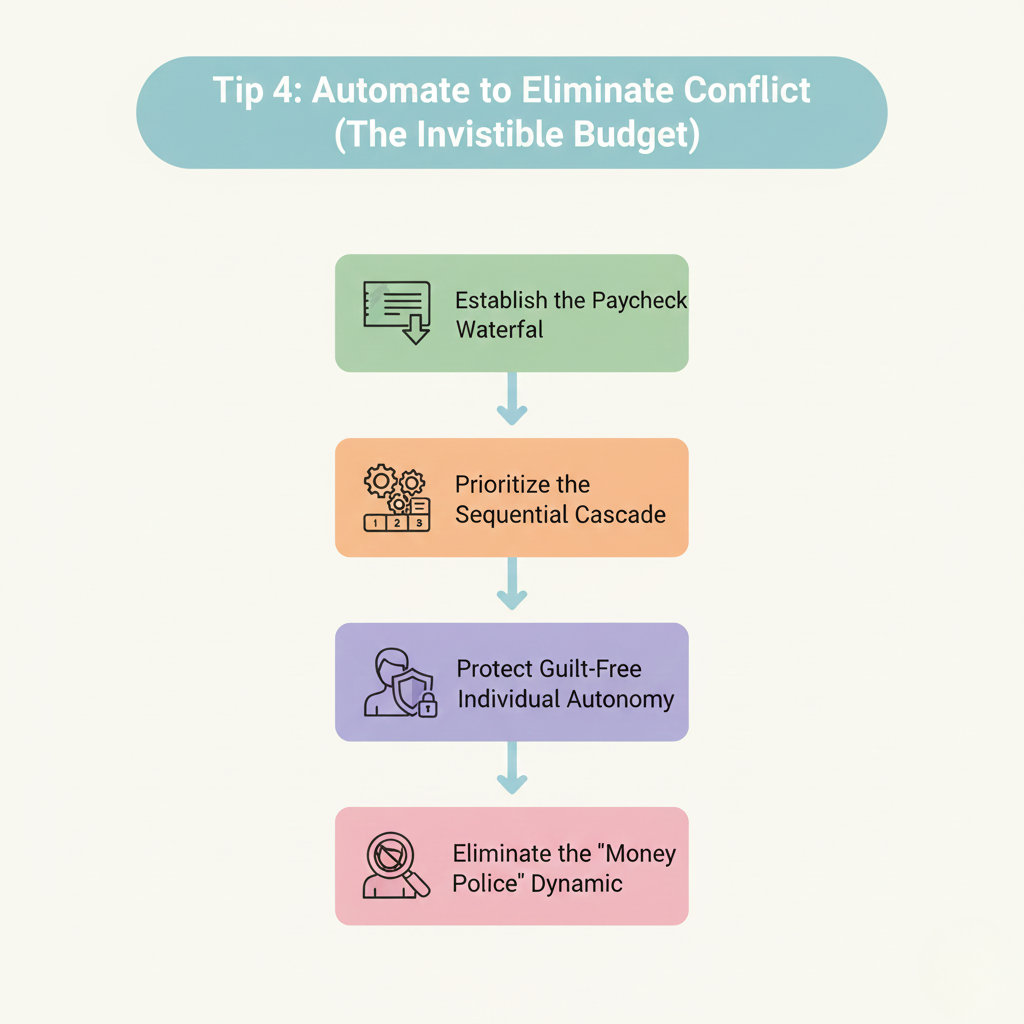

🔻 Tip 4: Automate to Eliminate Conflict (The Invisible Budget)

Automation is the single most powerful tool for preserving relationship harmony by removing human error and continuous negotiation from the budget process. The goal is to establish a self-running financial ecosystem where money management becomes functionally invisible.

The Paycheck Waterfall: Step-by-Step Automation Guide

The system must be set up so that contributions to goals and protection occur first, ensuring the couple invests in their future automatically. The critical timing requires setting up automatic transfers from both paychecks on the same day every month, ideally the day immediately following the receipt of both paychecks.

The transfers should follow this cascade sequence:

- Investment Contributions (10%): Funds are transferred first, maximized into tax-advantaged accounts based on whichever partner receives better employer matching benefits.

- Savings Goals (5–10%): Funds are transferred next into the Joint Savings account and its sub-accounts for specific goals.

- Guilt-Free Spending (20–35%): Each person’s allocated discretionary money is transferred simultaneously into their respective Individual Spending Accounts.

- Fixed Costs: The remaining balance in the Joint Checking Account is used to cover all automated fixed-cost payments (rent, utilities, etc.).

The Power of the Automatic Transfer: Making Money Management Invisible

The long-term impact of this level of automation is profound. When contributions to investments and shared goals are handled automatically, the emotional burden associated with the choice to “save enough” is completely lifted. The couple is guaranteed to be funding their shared future first.

Furthermore, once the automatic transfers are complete, the money deposited into the individual accounts is truly guilt-free. This radically reduces the opportunity for conflict, eliminating the need to ask for “permission” or justify personal purchases. Since the money fights that poison relationships are typically rooted in chronic, unresolved issues of trust and micro-management, removing the daily transaction monitoring structurally addresses the relationship’s crucial need for resolution and sustained peace.

🔻 Tip 5: Budgeting for Specific Life Stages and Income Disparity

No standard allocation model will fit every couple. A truly robust budgeting system must offer custom solutions for common financial imbalances and unique life stages.

Equity Over Equality: The Pro-Rata Split for Unequal Incomes

When a significant income disparity exists, the traditional 50/50 split of shared expenses often leads to systemic unfairness. A strict 50/50 division disproportionately depletes the lower earner’s income, leaving them with far less discretionary money and creating a power imbalance within the relationship.

The fairness solution is the proportional, or pro-rata, contribution method. If one person earns 70% of the combined household income, they contribute 70% of the shared expenses (fixed costs). This method ensures that after contributing to the partnership, both partners retain an equitable amount of their income for individual spending and savings. Implementing the pro-rata split fosters mutual respect and maintains financial independence for both partners, directly addressing the potential for one partner to feel “suffocated” by the shared financial constraints.

The DINK Advantage: Maximizing Investment Velocity

Dual Income, No Kids (DINK) couples possess a unique financial edge. Without the significant costs associated with raising children, DINK households benefit from 20 to 30% more discretionary funds compared to parents. This advantage is reflected in net worth metrics: DINK households aged 35 to 44 often have a median net worth approximately 75% higher than counterparts with children in the same age bracket.

The strategic imperative for DINK couples is to prioritize aggressive investment over simple cash management. They should push their investments bucket well beyond the standard 10% allocation and rigorously maximize tax-advantaged accounts (such as 401ks, IRAs, and Health Savings Accounts). This focus on wealth allows many DINK couples to achieve Financial Independence (FI) and retire 10 to 15 years earlier than the national average. Failing to plan strategically can easily lead to lifestyle inflation, eroding this unique advantage.

Facing significant shared debt can be overwhelming, triggering reminders of failure. However, major financial adversity is not insurmountable. Lessons from those who have successfully conquered large debts emphasize that recovery relies on a strong, shared mindset and the consistent execution of small, deliberate actions.

The action plan requires tackling debt as a primary, shared goal funded through the Joint Savings bucket. The couple must maintain total transparency regarding debt balances and creditor communications. Building financial trust in this scenario involves consistently contributing to the debt payoff goal, proving reliability, and communicating proactively if contributions become difficult. The Conscious Spending Plan supports this by allowing couples to temporarily reduce discretionary spending to accelerate the debt elimination timeline.

🔻 Tip 6: Choose Your Co-Pilot: Leveraging Modern Budgeting Tech

The right budgeting technology acts as a co-pilot, dramatically improving clarity and coordination and ensuring the automated flow established in Tip 4 functions smoothly. The selected tools must support the methodology focusing on tracking shared cash flow and aggregating net worth, rather than forcing manual, restrictive categorization.

Comparing Subscription Budgeting Tools (Monarch Money vs. YNAB)

While numerous budgeting applications exist, premium subscription tools offer the robust synchronization, and collaboration features necessary for high-functioning couple finance. Monarch Money and You Need a Budget (YNAB) represent two distinct but leading methodologies:

Budgeting App Comparison for Couples (YNAB vs. Monarch Money)

| Feature | Monarch Money | You Need a Budget (YNAB) | Advantages for Couples |

| Budgeting System | Cash Flow or Envelope (Flexible) | Zero-Based/Envelope (Strict) | Flexibility suits couples with varied financial habits |

| Shared Access | Yes (Partner collaboration features) | Yes (Up to 6 users) | Designed for modern partnership collaboration |

| Automation & Insights | Advanced Dashboards, AI Assistant, Forecasts | Minimal Automation Requires Manual Assignment (No Forecasts) | Superior visual snapshot and less manual chore work |

| Investment Tracking | Comprehensive (Ideal for wealth builders) | Moderate/Basic | Best for couples focused on net worth aggregation |

| Annual Pricing | $99.99/year (7-day trial) | $109/year (34-day trial) | Slightly better value proposition for comprehensive features |

Monarch Money offers superior value for couples focused on wealth building beyond mere expense tracking. Its modern interface, advanced visual dashboards, AI-powered insights, and net-worth tracking capabilities make it ideal for seeing the complete financial picture. YNAB, conversely, is the established gold standard for disciplined, zero-based budgeting, best suited for couples who require strict control and motivation through manual assignment of every dollar to build strong habits. For couples implementing the high-automation CSP (Tip 4), Monarch Money’s collaborative features and focus on wealth aggregation align more effectively with the goal of managing money invisibly.

Expense Trackers for Irregular Spending (Splitwise and Honeydue)

For managing irregular or non-fixed joint spending such as the cost of a shared vacation, an expensive dinner, or splitting supplies specialized expense trackers are essential complements to the 3-Account Strategy.

Honeydue is designed specifically for couples and allows partners to track joint and individual balances. Splitwise is particularly effective for organizing shared bills for households and group activities. Its primary strength is its ability to simplify complex debts into the easiest repayment plan, removing the inherent stress and awkwardness associated with calculating exactly “who owes who” when bills are paid unevenly. Using these tools prevents minor transactional disagreements from escalating into major relationship problems.

🔻 Tip 7: The Habit of Commitment—Building Resilience and Legacy

The final step in couples budgeting is the institutionalization of consistent commitment and the strategic mitigation of risk. Financial success is measured not just in accumulated cash, but in the sustained Coordination, Communication, and Confidence of the partnership.

Scheduling the Strategic Money Date (Review, Don’t Argue)

A financial system only remains effective if it adapts to the couple’s evolving circumstances. The entire Conscious Spending Plan must be reviewed and adjusted every six months, or immediately following major life changes such as a job change, moving, or starting a family.

This review should occur during a scheduled “Money Date,” reinforcing Coordination. This date is strictly for strategy reviewing investment growth, tracking savings goals, and deciding if the spending percentages need adjustment due to external factors (Tip 3). The core rule of the Money Date must be enforced: it is a critique of the system, not a critique of the partner. All discussions of individual, guilt-free spending are permanently off-limits, thereby ensuring the meeting remains productive and does not regress into the poisonous dynamic of financial conflict.

Beyond the Rainy Day: Funding the Emergency Moat

Neglecting the emergency fund is one of the major financial mistakes couples make. A robust budget prioritizes funding a protective buffer ideally three to six months of fixed costs—held within the Joint Savings account.

This fund serves as a crucial relationship protection mechanism. Economic forecasts often indicate periods of uncertainty, such as market volatility and shifts in growth rates. By fully funding an emergency moat, the couple protects their relationship from external economic shocks, such as unexpected job loss or market slowdowns, preventing financial stress from immediately triggering the intense, unresolved arguments that characterize money conflicts. This resilience maintains the couple’s feeling of Confidence.

The Unthinkable Mistake: Neglecting Protection and Legacy

Once cash flow is managed and goals are being funded, the highest priority shifts to risk mitigation. Neglecting critical protection mechanisms like life insurance, disability insurance, and formal estate planning is a serious financial mistake for couples. Comprehensive financial planning requires establishing wills, durable power of attorney, and necessary insurance to protect against the “unthinkable”.

Furthermore, couples should strategically utilize the “Divide and Conquer” approach for financial duties. One partner might focus on managing day-to-day bills, while the other handles investments, insurance, and long-term planning. Research concludes that this model is highly effective because it ensures that if one partner passes away, the survivor is already accustomed to managing half the workload, reducing the immense stress of suddenly adjusting to 100% of the financial responsibilities during a period of grief. This strategic division ensures the couple is always operating with institutionalized Clarity and Commitment.

Conclusion: Measuring Success in Connection, Not Cash

The journey to financial harmony for couples is a behavioral and psychological process, not a mathematical one. The most successful couples recognize that the ultimate objective of budgeting is not achieving perfection in tracking expenses but designing a self-sufficient system that minimizes friction and maximizes trust.

By implementing the hybrid account structure (Tip 2), adopting the automated Conscious Spending Plan (Tip 3 and 4), and committing to strategic, judgment-free communication (Tip 1 and 7), couples transform money from a source of destructive, unresolved conflict into a powerful catalyst for their shared future. The truest metrics of success are the quality of communication and the unshakeable shared confidence in the financial trajectory. Couples who budget together report higher satisfaction with communication on financial matters, proving that when the system works invisibly, the partnership thrives openly.

Alex Rodriguez specializes in simplifying investing and financial planning so beginners can feel confident taking their first steps. With a background in finance and a passion for financial literacy, he breaks down topics like index funds, retirement accounts, and long-term wealth-building into plain language and realistic action plans. At Dollar Pioneer, Alex creates guides and tools that help readers understand their options, compare strategies, and build investment habits that support their long-term goals, not just quick wins.