24 Even Number Savings Challenge Tactics to Bank

You stare at your bank balance. It is three days until payday. The number is lower than you thought. You feel that familiar knot in your stomach. We have all been there. The financial gurus tell you to stop buying coffee. They say you should make a budget. Those methods feel like punishment. You try them for a week. You fail. You feel guilty.

The problem is not your willpower. The problem is friction. Traditional saving hurts because it feels like a loss. You are taking money away from your “fun” pile and locking it in a “boring” pile. Your brain resists this. You need a system that feels like a game. You need a trigger that happens automatically.

This is where the Even Number Savings Challenge changes the game. It uses simple math to bypass your brain’s pain center. You do not have to make big decisions. You just look for even numbers.

I used these exact methods to save for a down payment on my first rental property. I did not earn a massive salary. I just tricked myself into saving money I did not miss. I have tested these strategies on friends and clients. The results are real. You can save $500 or $10,000 depending on how aggressive you get.

This guide covers 24 specific variations of this challenge. We will look at the math. We will look at the tools. We will look at how to stop yourself from stealing the money back.

Let’s fix your finances.

Executive Summary

You are about to learn 24 specific ways to gamify your savings using even numbers. Most people fail at saving because they rely on motivation. Motivation is fickle. These tactics rely on rules.

We will cover manual cash strategies for those who use physical money. We will cover digital automation for those who never touch cash. You will see exactly how much each method saves over 12 months.

Here is what you will get from this guide:

- 24 distinct saving triggers based on even numbers.

- The exact math behind each method.

- Honest reviews of apps that automate this.

- Psychological tricks to keep your hands off the savings.

- A clear path to banking $1,000 to $10,000 this year.

You do not need to use all 24 methods. Pick one. Pick three. The goal is consistency. If you start today, you will have a safety net before you know it.

1. The Transaction Round Up Plus One

This is the most common entry point. Most banking apps offer a “round up” feature. You spend $4.50. The app rounds it to $5.00. It moves $0.50 to savings. That is standard. We are going to turbocharge it.

The Standard Round Up is too slow. You might save $15 a month. You will barely notice that. The “Plus One” method adds a twist. Every time you round up to an even dollar, you add an extra dollar.

If you spend $4.20, you round up to $6.00 instead of $5.00. The transaction ends in an even number. You save $1.80 instead of $0.80. This doubles your savings rate without feeling like a huge hit.

The Math: Average 30 transactions a month. Standard Round Up: $15 saved. Plus One Round Up: $45 saved. Yearly Total: $540.

Pro Tip: Use an app like Qapital or Oportun. They allow custom rules. Set a rule that says “If purchase amount is even, save $2.”

2. The Even Date Transfer

Check the calendar. Is today an even numbered date? The 2nd, 4th, 6th, or 28th? If yes, you transfer a set amount.

This works because it is frequent. It happens 15 times a month. You cannot forget it. You can set a recurring alarm on your phone for 9 AM every other day.

Start small. Transfer $2 on every even day. It sounds like nothing. That is the point. You will not miss $2.

The Math: $2 per even day x 15 days = $30 month. Yearly Total: $360.

Want to hit $10,000? Make it $56 on every even day. Yearly Total: $10,080.

3. The 52 Week Evens Climb

You have seen the standard 52-week challenge. You save $1 on week one, $2 on week two. It gets brutal at the end. In December, you are trying to save hundreds of dollars right when you need money for gifts.

We modify this. We only use even numbers. Week 1 you save $2. Week 2 you save $4. Week 3 you save $6. You cap it at $100. Once you hit saving $100 a week, you stay there. Or you cycle back down.

This prevents the “December Crunch.” It keeps the amounts manageable for average earners.

The Math: Weeks 1 through 50 (increasing by $2) = $2,550. Yearly Total: $2,550+.

4. The Payday Even Split

This is for the high earners. This is for people who want to save $10,000 fast. Look at your paycheck net deposit. It is rarely a round number. It might be $2,456.78.

You keep the even hundreds. You save the rest. In this example, you keep $2,400. You transfer $56.78 to savings. Wait. That is the “Odd Split.” Let’s flip it for the “Even Split.”

You look at the last digit of your paycheck. If it is even ($2,456), you save a fixed percentage. Let’s say 10%. If it ends in an odd number ($2,457), you save 5%. This turns your savings rate into a game of chance. You find yourself rooting for an even paycheck.

The Math: Based on $50,000 net income. Average 50/50 split on odd/even paychecks. Yearly Total: $3,750 (approximate).

5. The Grocery Receipt Match

Grocery shopping is a budget killer. We often overspend. This method acts as a tax on your bad habits.

Look at your receipt total. Is the dollar amount even? (e.g., $142.xx). If yes, you save $10. If no ($143.xx), you save $20.

Wait. Why save more on the odd number? Because we want to reward the Even Number. We want “Even” to be the winner. When you hit an even number at the register, you get off easy. When you hit odd, you pay a penalty to your savings account.

This makes you watch the register. You might throw in a pack of gum to make the total even. You are engaging with your spending.

The Math: Weekly shop. 26 “Even” weeks ($10) = $260. 26 “Odd” weeks ($20) = $520. Yearly Total: $780.

6. The Tuesday/Thursday Lock

Tuesdays and Thursdays are even days of the week (2nd and 4th). This is a spending fast challenge.

On Tuesdays and Thursdays, you spend zero dollars. Nothing. No coffee. No lunch out. No Amazon purchases.

If you succeed, you transfer $20 to savings on Friday morning. If you fail and spend money, you transfer $0.

This builds discipline. It breaks the habit of daily consumption.

The Math: Success rate of 80% (you are human). 83 successful fasts x $20. Yearly Total: $1,660.

7. The Even Mileage Bounty

Do you drive? This one is fun. Check your odometer on Sunday night. Look at the last digit.

Is it even? Transfer $0.10 for every mile driven that week. Is it odd? Transfer $0.05 for every mile.

Again, we are gamifying the variable. If you drive a lot, this adds up fast. It also makes you conscious of how much you drive. It might save you gas money too.

The Math: Average 200 miles a week. Mix of rates. Yearly Total: $780.

8. The Weather Wager

This sounds crazy. I love it because it connects you to the physical world. Check the temperature high for the day.

Is it an even number? (72 degrees). Save that amount. $72? No. That is too much for most. Save the digits added together. 7+2 = $9. Or save $7.20.

If the temp is odd (73 degrees), you save nothing.

This works great in summer. It makes a hot day feel productive.

The Math: Varies wildly by location. Average $4 saved, 15 days a month. Yearly Total: $720.

9. The Even Serial Number Game

This is for cash users. You have a $5 bill in your wallet. Look at the serial number. Does it end in an even number?

If yes, you cannot spend it. You must put it in a jar when you get home. If no, you can spend it.

This is the “Liars Poker” of savings. It creates scarcity in your wallet. You might have $40 cash, but if three bills are “Evens,” you effectively only have $10 to spend. You will think twice about breaking a $20 if you know you might have to save the change.

The Math: One $5 bill saved per week. Yearly Total: $260.

10. The Sports Score Spread

Do you watch football or basketball? Pick a team. When they play, look at their final score. Is it even? Save $10. Is it odd? Save $5.

Did they win? Double it.

This associates positive emotions (your team winning) with saving money. You stop seeing saving as a loss. You start seeing it as a victory lap.

The Math: Based on an NFL season + NBA games. Yearly Total: $400 to $800 depending on team performance.

11. The Even Hour Rule

This is a behavioral restrictor. You are only allowed to make non-essential purchases during even numbered hours. 2 PM, 4 PM, 6 PM.

If you want to buy those shoes at 3:15 PM, you have to wait 45 minutes. Impulse buys die when you make them wait. If you still want it at 4:00 PM, buy it. But you must also pay a “patience tax” of $2 to your savings.

Most people just close the tab. They save 100% of the money by not spending it.

The Math: Saved purely by not spending: $1,000+. Patience tax revenue: $100. Yearly Total: $1,100+.

12. The Even Check Number

I rarely write checks. Maybe you pay rent with checks. Look at the check number (e.g., #104). If it is even, round up the payment amount in your register and move the difference. Rent is $1,200. Check is #104. Move $104 to savings? No. That is too steep. Move $10.40.

If the check number is odd, you save nothing.

The Math: 12 checks a year. 6 even. Yearly Total: $62.40 (Small, but it all counts).

13. The Even Dollar Dining Out Tip

When you eat out, you leave a tip. Make your total bill an even number. Bill is $43.20. You want to tip around 20%. Make the final total $52.00. The tip is $8.80.

Here is the saving part: You match the tip in your savings account. If you can afford to tip the server $8.80, you can afford to tip yourself $8.80.

If you cannot afford to match the tip, you cannot afford to eat out. That is a hard rule. It keeps you honest.

The Math: Dining out once a week. Average tip $10. Yearly Total: $520.

14. The “No Spend” Even Streak

Mark a calendar. Every day you spend $0 is a success. If you string together 2 days (even number), transfer $10. If you string together 4 days, transfer $20. If you string together 6 days, transfer $40.

The reward grows as the even number grows. This gamifies frugality. You will fight to keep the streak alive to hit that big payout.

The Math: Variable. Yearly Total: $300 – $600.

15. The Even Percent Raise

Did you get a raise this year? Maybe 3% or 4%? If the percent is even (4%), save half of the raise amount. If the percent is odd (3%), save all of the raise amount.

This combats lifestyle creep. When we get more money, we usually spend more. This rule forces you to capture the upside immediately.

The Math: $60,000 salary. 4% raise ($2,400). Save half ($1,200). Yearly Total: $1,200 (recurring forever).

16. The Step Counter Challenge

Most of us have smartphones or watches that count steps. Check your daily total. Did you hit an even thousand? (10,000, 12,000). If yes, pay yourself $5. If you landed on an odd thousand (11,300), pay yourself $1.

This encourages health and wealth. You will find yourself walking around the living room at 10 PM trying to cross the 10,000 mark so you can “earn” your $5 deposit.

The Math: Hit goal 3 times a week. Yearly Total: $780.

17. The Even Year Vintages

This is for wine or whiskey drinkers. Or even coin collectors. When you buy a bottle or item, look at the year. Is it an even year? 2018? 2022? Add a 10% surcharge to the price and bank it. Bottle costs $20. Year is 2018 (Even). Price is now $22. Put $2 in savings.

This is a luxury tax. It only applies to discretionary items.

The Math: Variable based on consumption. Yearly Total: $100 – $300.

18. The Social Media “Even” Scroll

Check your screen time report on Sunday. Look at the minutes spent on Instagram or TikTok. Is it an even number? (e.g., 42 minutes daily average). Penalty: $1 per minute over 30. If you averaged 42 minutes, that is 12 minutes over. You owe your savings account $12.

If it is an odd number, you owe half.

This hurts. It is supposed to hurt. It buys you back your time OR it builds your bank account. Win-win.

The Math: Based on average addiction levels. Yearly Total: $500+.

19. The Even Battery Charge

Plug your phone in at night. Look at the percentage. Is it exactly even? 14%? 22%? Transfer that amount in cents. $0.22. If it is odd, transfer nothing.

This is a micro-habit. It requires zero brainpower. It barely costs anything. But it keeps the habit of “opening the banking app” alive. The habit is more important than the amount.

The Math: Yearly Total: $40. (Low impact, high habit building).

20. The Grocery Item Count

Count the items in your cart before checkout. Do you have an even number of items? 24 items? You are safe. Do you have an odd number? 25 items? You must put one back. Or, pay a $5 penalty to savings.

This stops you from grabbing random candy bars at the checkout. It forces intentionality.

The Math: Savings from items not bought: $200. Penalty savings: $50. Yearly Total: $250.

21. The Even Gas Pump Game

You are pumping gas. Try to stop the pump on an exact even dollar amount. $40.00. If you hit it perfectly, reward yourself. Transfer $5 to your “Fun Fund.” If you miss it ($40.01), punish yourself. Transfer $5 to your “Boring Emergency Fund.”

This makes a mundane chore interesting.

The Math: Weekly fill up. You will miss often. Yearly Total: $150.

22. The Subscription Purge (Even Months)

On even numbered months (February, April, June…), you must cancel one subscription. Netflix. Hulu. That gym membership you never use. Take the cost of that subscription and set up an auto-transfer for that amount.

You cancel a $15 streaming service. You set up a recurring $15 transfer. You kept the expense, but you are now paying yourself.

The Math: Cancel 3 services a year avg $12. Yearly Total: $432.

23. The “Found Money” Evens

You find a $20 bill in a jacket pocket. You get a $50 rebate check. You sell something on Facebook Marketplace for $40. If the amount is even, you keep 50% and save 50%. If the amount is odd ($25), you save 100%.

We prioritize Evens again. Evens let you spend. Odds make you save.

The Math: Variable. Yearly Total: $300+.

24. The Double Down Even Year

This is the nuclear option. Is the current year an even number? (2026). Yes. That means you double your standard savings contributions. If you normally do $100 a month into your IRA, you do $200.

You only do this for one year. Then you can rest on the odd year. This works well for freelancers who have boom and bust years.

The Math: Base savings $200/mo. Doubled to $400/mo. Yearly Total Increase: $2,400.

How to Automate This (So You Actually Do It)

Willpower fails at 9 PM on a Tuesday. You need robots to do this for you. Here are the tools I trust.

The Best Apps for Rules

- Qapital: This is the gold standard for “If This, Then That” banking. You can set the “Weather Rule” or the “step counter rule” directly in the app. It links to your main bank. It pulls the money automatically.

- Cost: small monthly fee. Worth it.

- Chime: Great for the “Round Up” and “Payday Split.” It is a full bank account. Their round-up feature is aggressive.

- Oportun (formerly Digit): It uses AI to study your checking account. It finds money you won’t miss. It is not strictly “Even Number” based, but it follows the same philosophy of painless saving.

The Analog System (Cash Jars)

If you use cash, you need physical jars. Label them. “The Even Jar.” Do not use a clear jar. Use an opaque one. If you see the money, you will spend it. If you cannot see it, it does not exist until you break the jar.

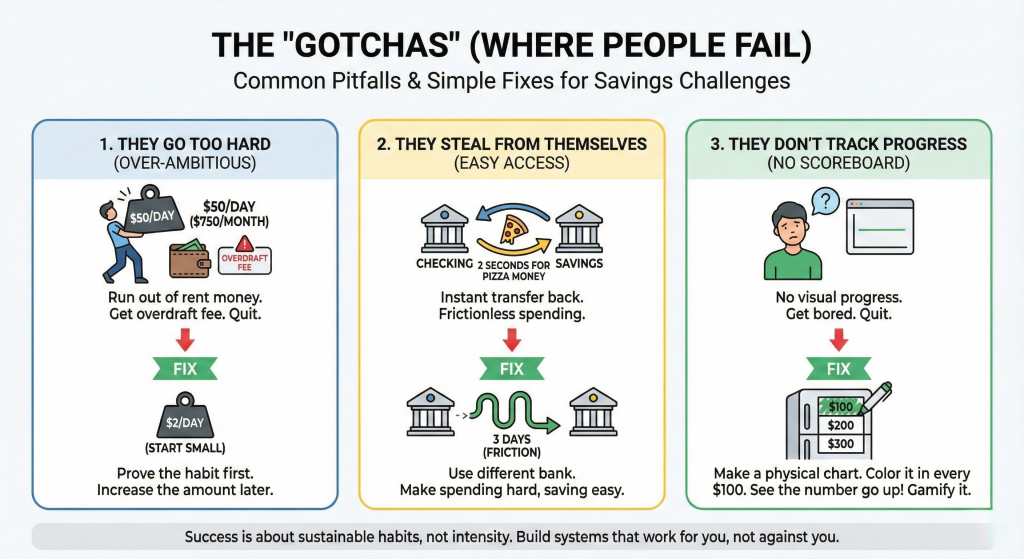

The “Gotchas” (Where People Fail)

I have seen people start this and quit in three weeks. Here is why.

1. They Go Too Hard

They pick “The Even Date Transfer” and set it to $50. That is $750 a month. They run out of money for rent. They get an overdraft fee. They quit. Fix: Start with $2. Prove the habit first. Increase the amount later.

2. They Steal From Themselves

The savings account is connected to the checking account. It takes two seconds to transfer the money back when they want pizza. Fix: Use a different bank for savings. Make the transfer take 3 days. Friction works both ways. Make saving easy and spending hard.

3. They Don’t Track Progress

Gamification needs a scoreboard. If you do not see the number going up, you get bored. Fix: Make a physical chart on your fridge. Color it in every time you hit $100.

FAQ: Common Questions About Even Number Savings

Is this better than the 52-Week Challenge? Yes. The 52-Week Challenge is flawed because the hardest weeks are in December. The Even Number tactics are consistent year-round. They spread the load.

Can I do this if I have debt? If you have high-interest credit card debt (20%+), pay that first. Use the “Even Number” triggers to make extra debt payments instead of saving. The math is the same. The destination is just different.

What if I get paid irregularly? Use Method #1 (Transaction Round Up) and Method #4 (Payday Split). These scale with your activity. If you earn $0, you save $0. If you earn $5,000, you save a lot. It protects you during lean months.

Which method saves the most money? Method #24 (Double Down) saves the most but requires the most income. Method #1 (Round Up Plus One) is the best balance of “painless” and “effective” for most people.

Is this safe? The apps mentioned (Qapital, Chime) are FDIC insured. Your money is safe. If you use a physical jar, hide it well.

Conclusion

You do not need to be a math genius to save money. You do not need a six-figure salary. You just need a system that outsmarts your own impulses.

The Even Number Savings Challenge is not about the numbers. It is about the attention. It forces you to look at your money every day. It forces you to pause before you spend. That pause is where wealth is built.

Pick one method from the list above. Just one. Set it up today. Check back in 30 days. You will see a balance you didn’t think was possible.

Which one are you going to try? The “Round Up Plus One”? The “Weather Wager”? Commit to it. Your future self is waiting for that deposit.

Jason Lee blends real-world budgeting experience with creative savings strategies shaped by his background in community outreach and financial education. He specializes in building practical systems—like zero-based budgets, sinking funds, and spending trackers—that regular families can actually stick with month after month. At Dollar Pioneer, Jason focuses on user-friendly guides, printables, and templates that make smart money management more accessible, less intimidating, and easier to turn into a weekly habit.