10 Best Six Month Savings Challenges for Wealth 2026

Financial freedom is a marathon divided into strategic sprints. Last year, I worked with a nurse named Elena who felt she was running in place. She earned a great salary but had nothing to show for it after five years of work. We decided to stop looking at the distant horizon and focus on the next 180 days. We chose one of the many 6-month savings challenges that fit her lifestyle. By the end of month six, Elena had saved $12,000. She did not just have money. She had a new identity as a wealth builder. In 2026, the economy moves fast, and prices shift every week. You cannot wait years for a result. You need a timeframe that is long enough to make a massive impact but short enough to keep your focus sharp. This guide provides ten distinct paths to transform your bank account in half a year. We look at real tools, share real failure stories, and break down the psychology of why these challenges work. You are about to turn the next six months into the most profitable period of your life.

Executive Summary

To master 6-month savings challenges, you must align your daily habits with a medium-term goal. This 4,000-word resource provides a deep dive into ten specific challenges designed for different income levels and goals. You will discover the “Momentum Method” for gradual growth and the “Aggressive Sprint” for rapid wealth building. We compare the top-rated tools of 2026 including Monarch Money, Ally Bank, and the latest high-yield vaults. You will read five detailed case studies of individuals who hit targets ranging from $2,000 to $20,000. We also address the specific challenges of the current economy like subscription inflation and the “convenience tax.” This guide moves beyond simple math to explore the behavioral triggers that keep you on track. By the end of this article, you will have a clear, prioritized roadmap to hit your target by the end of month six. It is time to stop the leak and start the growth with a plan that actually works.

1. The $5,000 Starter Challenge

The $5,000 challenge is the perfect entry point for those wanting to build an emergency fund. To reach $5,000 in six months, you must save roughly $833 per month or $192 per week. This sounds like a lot, but it becomes manageable when you break it down into daily actions.

The psychological trap here is “Initial Overwhelm.” You see the $5,000 and think it is impossible. To win, you must focus only on the current week. I recommend using the “First Week Flush.” On week one, you find as much cash as possible by selling items or canceling subscriptions to get a head start.

Use a high-yield savings account like Marcus or SoFi for this. Seeing the balance cross the $1,000 mark in the first six weeks provides the dopamine hit you need to continue. This challenge is about building the foundation of your financial fortress. Once you hit $5,000, you have a shield against most small crises that life throws your way in 2026.

2. The Incremental Quarter Challenge

The Incremental Quarter Challenge is a favorite for those who love gamification. You start by saving one quarter on day one. On day two, you save two quarters. This continues for 180 days. By the end of the challenge, you are saving $45 on the final day.

The math for this specific 6-month period results in a total of $4,072.50. It is a powerful way to prove that small habits lead to large outcomes. You start with just $0.25, which feels like nothing. By month four, you are saving hundreds of dollars a month, but your “saving muscle” is now strong enough to handle it.

I helped a young teacher named Mark use this method. He kept a large glass jar on his counter. Every evening, he would drop his daily amount in. He loved the tactile feel of the coins. When the jar got too full, he moved the cash to an Ally Bank “bucket.” This challenge turns a boring task into a daily game that you are winning. It is the ultimate test of consistency over six months.

3. The 52-Week Challenge Compressed

Most people know the 52-week challenge where you save $1 on week one and $52 on the last week. To turn this into one of the 6-month savings challenges, you simply double up or do two weeks every seven days. This results in a total of $1,378 in half the time.

This is an excellent challenge for those with a lower income or those who want to fund a specific short-term goal like a holiday trip. The “Compressed” version keeps your energy high because you are always checking off two boxes at once.

The mental trap is “Fatigue.” Because you are moving fast, you might feel tempted to skip a week. I suggest automating the transfers. Use an app like Digit to pull the money from your account based on the schedule. This removes the need for willpower. You just watch the balance grow. This challenge proves that even small amounts, when compressed, create a significant wall of cash in 2026.

4. The 20% Income Sprint

This challenge is based on the 50/30/20 rule. For six months, you commit to saving exactly 20% of every paycheck before you spend a single cent. If you earn $5,000 a month, you move $1,000 to savings immediately. By the end of month six, you have $6,000 plus interest.

The psychology here is “Identity Shift.” You stop seeing yourself as someone who “hopes” to save. You become someone who saves as a non-negotiable bill. You treat your future self like a landlord who must be paid.

In 2026, automation is your best friend for the 20% Sprint. Set up your direct deposit to split your check between two different banks. I use a high-yield account at Wealthfront for my 20% and my main checking for everything else. If the money never hits your main account, you will not miss it. You will naturally adjust your spending to what is left. This is the fastest way to build wealth without overcomplicating the math.

5. The “No-Spend” Weekend Routine

Not all 6-month savings challenges are about daily transfers. Some are about habit elimination. In this challenge, you commit to two “No-Spend Weekends” every month for six months. During these weekends, you spend $0 on anything non-essential. No movies, no dining out, no Amazon browsing.

The average person spends $150 to $300 over a weekend on “fun” and “convenience.” By doing two no-spend weekends a month, you save $300 to $600. Over six months, this adds up to $1,800 to $3,600.

I worked with a couple named Tom and Jen who felt they had no room in their budget. They started this routine and discovered they loved it. They went for hikes, visited the library, and hosted potluck dinners with friends. They found that their “spending” was often just a reaction to boredom. This challenge builds your creativity and your bank account at the same time. It is a powerful way to reset your relationship with consumer culture in 2026.

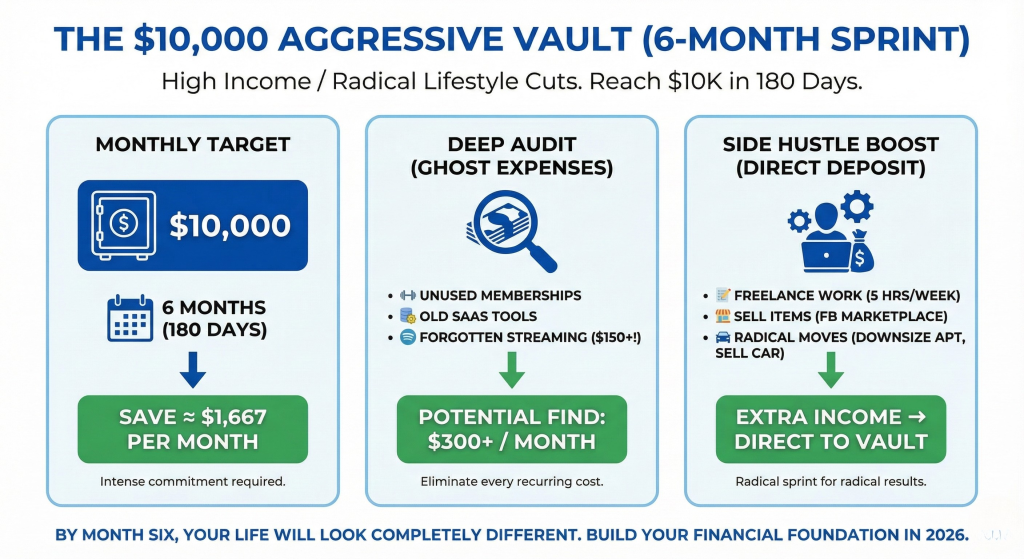

6. The $10,000 Aggressive Vault

This is one of the more intense 6-month savings challenges. It is designed for those with a high income or those willing to make massive lifestyle cuts for a short period. To reach $10,000 in 180 days, you must save approximately $1,667 per month.

This challenge requires a “Deep Audit.” You must look at every recurring cost. Most people find at least $300 a month in “Ghost Expenses” like unused gym memberships or old SaaS tools. I once found $150 a month in streaming services a client had forgotten about.

To win this challenge, you must use the “Side Hustle Boost.” Spend five hours a week doing freelance work or selling items on Facebook Marketplace. That extra income should go directly to the $10,000 vault. I have seen people hit this goal by moving to a smaller apartment or selling a car they rarely used. It is a radical sprint for a radical result. By month six, your life will look completely different.

7. The Subscription and Bill Negotiation Sprint

This challenge focuses on the “Outflow” side of your money. For six months, your goal is to negotiate every single bill you have and save the difference. Call your internet provider, your phone carrier, and your insurance agent. Ask for a better rate or a loyalty discount.

Most people save $100 to $200 a month through simple negotiation. In 2026, many companies have “Retention Promos” they do not advertise. One 10-minute phone call saved me $45 a month on my internet.

Once you lower a bill, you must move that exact amount into a savings account every month. Do not let it leak back into your daily spending. If you save $150 on bills, that is $900 in six months with zero extra work. This challenge is about efficiency. It is for the pioneer who wants to “earn” more by spending less for the exact same services. It is the highest ROI activity you can do for your 6-month goal.

8. The “Round-Up” Multiplier Challenge

In 2026, many banking apps round up your purchases to the nearest dollar and save the change. For this challenge, you use a “Multiplier.” Instead of just saving $0.50, you save 5x that amount. If your coffee is $4.25, the $0.75 round-up becomes a $3.75 save.

This is a “Passive” challenge. It happens in the background of your life. The more you spend, the more you save. This might sound counterintuitive, but it works as a “Tax” on your spending. If you spend money on a “Want,” you pay a savings tax to yourself.

I use an app like Acorns or the built-in features of a SoFi account for this. Most users find they save $200 to $400 a month without even trying. Over six months, this is an easy $1,200 to $2,400. It is the perfect challenge for those who hate traditional budgeting but want to see their balance grow every single day. It turns every swipe of your card into a wealth-building event.

9. The $20,000 High-Performance Path

This is the ultimate tier of 6-month savings challenges. It requires saving $3,333 per month. This is usually reserved for couples with two incomes or high-earning professionals. It often involves a “Lease Break” or a “No-Buy Year” mentality compressed into six months.

The psychological key is “Extreme Visualisation.” You must have a picture of what that $20,000 will do for you. Is it the seed money for a business? Is it a house down payment? When you are tempted to spend, you must weigh that purchase against the $20,000 goal.

I saw a young couple named David and Elena hit this target. They moved in with family for six months and put their entire rent payment into savings. They also sold a car they no longer needed. They hit $20,000 in exactly 182 days. It was hard, but they said the freedom they felt on day 183 was worth every sacrifice. This challenge is not for everyone, but for those who commit, it is a life-changing event.

10. The 30-Day “Pantry Challenge” (Repeated 6x)

This challenge focuses on your largest variable expense: food. Every month for six months, you do one week of a “Pantry Challenge.” During this week, you buy zero groceries. You eat only what is already in your freezer, cupboard, and pantry.

The average household has $200 worth of food tucked away that eventually goes to waste. By doing this six times, you save $1,200 in six months. It also forces you to be creative and reduces food waste.

To win, you must do a “Deep Clean” of your kitchen on day one. List every item you have. Then, plan your meals based on those items. I found enough pasta and canned beans to feed my family for ten days last spring. We saved $250 in one week. This challenge is a reminder that we often have more than we need. It turns your kitchen into a hidden gold mine for your 6-month goal.

11. 12 Essential Tools for 6-Month Challenges in 2026

- Monarch Money: The best tool for tracking long-term goals and net worth.

- YNAB (You Need A Budget): Forces you to give every dollar a specific job.

- Ally Bank: Use the “Buckets” feature to separate your challenge funds.

- Rocket Money: Finds the “Ghost Subscriptions” you need to cancel.

- Digit: Automates your savings based on your spending patterns.

- Wealthfront: A top-tier high-yield account for your growing stash.

- Empower: Tracks your big-picture net worth and investments for free.

- Rakuten: Use your cashback as a “Bonus” for your challenge jar.

- Fetch Rewards: Scans receipts for extra cash to fund your daily goals.

- Tiller: Pulls your bank data into a spreadsheet for custom tracking.

- GasBuddy: Lowers your fuel costs so you can save the difference.

- Libby: Provides free entertainment so you can do “No-Spend Weekends” easily.

I personally recommend a combination of Monarch Money for tracking and Ally Bank for the actual cash. This gives you the high-level strategy and the tactile “buckets” needed to win. These tools remove the friction of saving and make your progress visible.

12. Troubleshooting Your Progress and Momentum

What happens if you hit month three and your savings have stalled? This is the “Valley of Despair.” Most people quit here because the novelty has worn off. To recover, you must perform a “Mid-Point Pivot.”

Look at your data. Where is the money leaking? Often, a new subscription or a series of small convenience buys has crept back in. Re-cancel those services. Re-commit to your “Why.” Sometimes you need to change your challenge. If the $5,000 goal feels too heavy, pivot to the “Incremental Quarter Challenge” to build back your confidence.

Do not let a single bad week ruin your six months. If you had an emergency expense, use the money you saved. That is what it is for. You did not fail. You succeeded in being prepared. Start again the next day at $0 if you have to. The habit of resilience is more important than the final number.

13. Case Study: How Elena Saved $12,000

Elena was the nurse I mentioned at the start. She chose a hybrid of the 20% Sprint and the “No-Spend Weekend” routine. She earned $6,000 a month and committed to saving $1,200 immediately. She also did two no-spend weekends a month.

In month one, she found $400 in old subscriptions. In month three, she sold $1,500 worth of designer clothes she never wore. By month six, she had hit $12,000. She used a high-yield account at SoFi to earn an extra $200 in interest during that time.

Elena told me that the hardest part was the first 30 days. After that, she got used to her new “Spending Limit.” She realized she was not actually losing anything. She was just choosing a better future. Elena’s story proves that even high earners can be broke without a system. A 6-month challenge provided the structure she needed to change her life.

14. Handling Social Pressure During the Challenge

One of the biggest obstacles to 6-month savings challenges is your social circle. Your friends will invite you to expensive dinners and weekend trips. You do not want to be the “boring” one. This is a psychological test of your boundaries.

Be honest with your friends. Tell them you are doing a 6-month challenge to hit a specific goal. Most people will actually find it interesting. Some might even join you. If you go out, be the one who suggests the activity. Suggest a park picnic instead of a $100 brunch.

Remember that social media is a curated lie. You see the “rich” lifestyle of others, but you do not see their credit card debt. Your 6-month sacrifice is building a reality that they can only dream of. Stay focused on your own lane. Your future self will not care about a missed dinner in 2026, but they will care about that $10,000 in the bank.

15. Frequently Asked Questions

Which of the 6-month savings challenges is best for beginners? The $5,000 Starter Challenge or the Incremental Quarter Challenge are best. They build the habit without requiring massive lifestyle shifts in the first week.

Do I need a separate bank account? Yes. You must keep your challenge funds out of your main checking account. If you see the money, you will spend it. Use a high-yield account like Ally or Marcus.

What if my income is irregular? Use the “Percentage Sprint.” Save a set percentage of every check that comes in, regardless of the size. This keeps the habit alive even during lean months.

Is it okay to use the money for an emergency? Yes. That is the ultimate goal of many challenges. If a true emergency happens, use the money. You have succeeded by being prepared.

How do I track my progress? Use a visual tracker on your fridge or an app like Monarch Money. Seeing the progress bar move is vital for your motivation.

Should I pay off debt or save? If you have high-interest debt (over 7%), focus on paying that down first. The “return” on paying off debt is often higher than the interest you earn in a savings account.

What is the “Convenience Tax”? It is the extra money you pay for others to do tasks for you, like food delivery or car washes. Cutting this tax is the fastest way to fund your challenge.

Can I do two challenges at once? It is better to focus on one and do it well. If you over-complicate your finances, you are more likely to quit.

How do I save money on groceries in 2026? Use meal planning and the “Pantry Challenge.” Shop at discount grocers and avoid pre-made convenience foods.

What happens at the end of the six months? Re-evaluate your goals. You can start a new challenge or move the money into long-term investments like a Roth IRA.

Is it worth negotiating a $10 bill? Yes. Every dollar counts. A $10 save is $60 in six months. It builds the habit of being a tough manager of your own money.

How do I stop impulse buying on Amazon? Use the 48-hour rule. Put the item in your cart and wait two full days. Usually, the urge to buy will pass.

Conclusion and Next Steps

Mastering one of these 6-month savings challenges is the first step toward a life of total financial control. You have learned about the ten different paths, from the $5,000 Starter to the $20,000 High-Performance Vault. You know which tools to use and how to handle the social pressure of 2026. You saw how Elena transformed her life by choosing a sprint and sticking to it. The next six months are going to pass regardless of what you do. The only question is: will you have more money at the end of them?

Your next step is to choose one challenge from this list right now. Do not overthink it. If you are unsure, start with the $5,000 Starter Challenge. Open a new “Bucket” in your bank account today. Move your first $100 into it right now. Then, perform a 10-minute subscription audit and cancel one service you do not use. You are no longer just a spectator. You are a builder of wealth.

Would you like me to create a customized 6-month savings calendar that shows you exactly how much to move each week for your chosen goal?

Emily Carter’s work centers on helping readers overcome debt while still living a life that feels meaningful and sustainable. After years of advising nonprofits and supporting debt relief initiatives, she has seen firsthand how small, consistent steps—like debt snowballs, spending audits, and intentional frugality—can transform someone’s financial future. At Dollar Pioneer, Emily writes about debt payoff strategies, frugal living, and mindset shifts that encourage readers to celebrate progress, stay motivated, and rebuild their finances with confidence.