How to Get Out of Debt for Good and Finally Breathe

The 2 AM Panic Is Real (And You’re Not Alone)

It’s 2:17 AM. The house is silent, but your mind is screaming. The credit card statement you shoved in a drawer last week is now a monster under the bed. You do the terrifying math in your head for the hundredth time. It never adds up. The weight on your chest feels physical, a crushing pressure that steals your breath and your sleep.

If this feels familiar, it’s because you are part of a quiet crisis. As of the first quarter of 2026, total U.S. household debt hit a staggering $18.39 trillion. That number is so large it’s meaningless, but the feeling it creates in millions of homes is brutally specific: fear, shame, and a sense of being utterly trapped. You are not alone in this feeling. Not even close.

I remember my own 2 AM panic. It was a Tuesday in 2018. A medical bill for $4,300 arrived, and I realized my “manageable” debt was a house of cards. The shame was suffocating. I felt like a failure, a fraud who was good at giving advice but terrible at living it. But that night, staring at the ceiling, I made a decision that changed everything. This guide is what I wish I’d had then.

Forget the generic advice to “just cut out lattes.” That’s an insult to your intelligence. Over the next 10 minutes, we’re going to dismantle the psychological traps that keep you in debt, choose the right tactical weapon for your personality, and build a step-by-step plan to reclaim your financial life. You will discover why your brain is wired to fail at this and how to rewire it for success. This is your first breath of fresh air. Let’s take it together.

Before We Touch a Spreadsheet, Let’s Address the Elephant in the Room: Your Brain

The biggest obstacle to getting out of debt isn’t math; it’s your mindset. Behavioral finance shows that emotional triggers, cognitive biases like loss aversion, and social pressure often lead to a cycle of borrowing and shame that no budget alone can fix.

For years, I thought getting out of debt was a numbers problem. It’s not. It’s a human problem. Studies have repeatedly shown that individuals struggling with debt are more likely to suffer from depression and anxiety. That financial stress manifests physical headaches, poor sleep, an inability to focus. It creates a state of chronic, low-grade panic.

In that state, we do what humans do best: we seek comfort. And in our modern world, comfort is just a click away. This is the vicious cycle of “emotional spending.” We feel stressed, bored, or inadequate, so we buy something to get a temporary hit of pleasure, only to feel a wave of regret and deeper financial anxiety moments later. That new anxiety then becomes the trigger for the next purchase.

The first, most critical step is to understand that debt isn’t a character flaw; it’s a behavioral pattern. The problem isn’t that you’re “bad with money.” The problem is that you might be using money to solve problems it was never meant to solve like healing from a bad day at work or curing a sense of loneliness. Attacking behavior is the only way to create lasting change. This reframes the entire battle from a moral failing to a solvable psychological puzzle, which is something you can absolutely win.

This brings me to a controversial but vital point: shame is your enemy, not your motivator. Let me be clear: shame is useless. It paralyzes you. It makes you hide the bills, ignore the calls, and pretend the problem doesn’t exist. Our first job is to replace shame with strategic, unemotional ownership. You are not your debt. It is simply a number on a page, and we are about to create a plan to make that number smaller.

Case Study 1: Sarah’s $22,000 “Revenge Spending” Cycle

Sarah, a client from last year, came to me with $22,000 in credit card debt. She had a good job but couldn’t understand where her money went. Her budget looked fine on paper. After a few sessions, we found the leak. Her trigger was a stressful weekly meeting with her boss. After every bad meeting, she’d go online and buy something nice: a new dress, expensive skincare as a form of “revenge” against her boss and the company. It was a temporary high followed by deep regret.4

The solution wasn’t a stricter budget. It was a new rule: after a bad meeting, she had to go for a 15-minute walk before she could open a shopping app. Nine times out of ten, the fresh air and physical movement dissipated the anger, and the urge to spend vanished. By addressing the trigger, we cut her impulse spending by over $800 a month. That money, redirected to her debt, became her weapon.

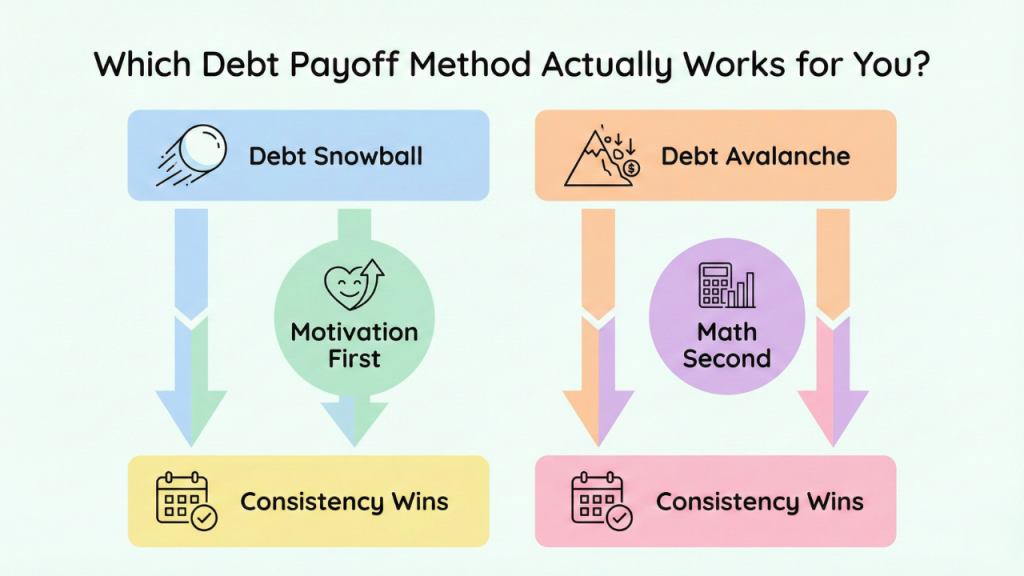

Which Debt Payoff Method Is Right for You? (Hint: Math Is a Trap)

The two best debt payoff methods are the Debt Snowball and the Debt Avalanche. The Snowball method focuses on paying off the smallest debts first for psychological momentum, while the Avalanche method targets the highest-interest debts first to save money.

This is the biggest debate in the debt-free world, and most “experts” get it wrong because they focus only on the math. Let’s break it down with a simple example. Imagine you have three debts:

- Credit Card: $500 balance at 22% interest

- Personal Loan: $3,000 balance at 10% interest

- Car Loan: $10,000 balance at 6% interest

The Debt Avalanche method, favored by financial purists, says you should make minimum payments on everything and throw every extra dollar at the credit card because its 22% interest rate is costing you the most money. Mathematically, this is the fastest and cheapest way to become debt-free.

The Debt Snowball method, popularized by Dave Ramsey, says you should ignore the interest rates. Make minimum payments on everything and throw every extra dollar at the smallest balance first the $500 credit card. Once it’s gone, you “roll” that payment onto the next smallest debt (the personal loan). The idea is that small, quick wins build momentum and keep you motivated.

So, which is better? I’m going to say what many financial experts won’t: for 90% of people drowning in debt, the Debt Avalanche is a terrible idea. It’s mathematically perfect and emotionally bankrupt. It asks you to run a marathon with no water stations for the first 20 miles. The Debt Snowball gives you a win in the first month or two. That dopamine hit is the fuel you need to keep going. A study published by the Harvard Business Review even confirmed that focusing on the smallest debt first helps keep motivation high. Personal finance is 80% behavior and 20% head knowledge. A plan you abandon is infinitely more expensive than a slightly less optimal plan you see through to the end. Choose the plan built for humans.

The Ultimate Debt Payoff Method Showdown

| Method | Core Principle | Best For (Personality Type) | Biggest Pro | Biggest Con (The Trap) |

| Debt Snowball | Pay off debts from smallest balance to largest, regardless of interest rate. | You need quick wins to stay motivated. You feel overwhelmed and need to see progress fast. | Creates powerful psychological momentum and simplifies focus. | You will pay more in total interest over the life of the loans. |

| Debt Avalanche | Pay off debts from highest interest rate to lowest, regardless of balance. | You are highly disciplined, motivated by numbers, and not easily discouraged by slow progress. | Mathematically optimal. Saves you the most money on interest. | It can be incredibly demoralizing as it might take years to pay off the first debt. |

| Hybrid Method | A blend of both. Start by knocking out one or two small debts (Snowball) then switch to the highest-interest debt (Avalanche). | You want an initial motivational boost but also want to optimize for interest savings long-term. | Gets the best of both worlds: early motivation and long-term savings. | Requires you to switch strategies, which can be confusing for some. |

How to Build a “Real Life” Budget That Doesn’t Feel Like a Cage

A successful budget for debt payoff focuses on ruthlessly cutting discretionary spending while protecting essential needs. Use the zero-based budgeting method, where every dollar of income is assigned a job, ensuring that extra money is intentionally directed toward debt.

The word “budget” makes most people cringe. It sounds like a diet for your money, restrictive, boring, and doomed to fail. We’re not doing that. We’re creating a temporary, wartime spending plan. The goal isn’t to track every penny for the rest of your life; it’s to free up the maximum amount of cash to fire at your debt.

Here’s how to build your “Bare-Bones” budget:

- List Your Four Walls: This is your foundation. Rent/mortgage, utilities, food (groceries only, not restaurants), and essential transportation. These get paid first, no matter what.

- List Minimum Debt Payments: Gather every single bill and list the minimum payment required for each. This is the baseline you must meet to stay current.

- Cut Everything Else (Temporarily): Subscriptions you forgot you had, daily coffees, lunches out, streaming services, gym memberships. This is the “fat” we’re trimming. This isn’t forever. This is for a season. We’re performing financial surgery to save the patient.

- Calculate Your “Shovel”: Your monthly income minus (Your Four Walls + All Minimum Payments) equals your extra debt-fighting money. This is your weapon, your shovel to dig yourself out.

My favorite tool for this is You Need a Budget (YNAB). It’s built on the philosophy of zero-based budgeting, forcing you to “give every dollar a job”. It’s not cheap (around $109 per year as of 2026) and has a learning curve, but it can fundamentally change your relationship with money.

My first budget failed in a week because it was perfect… and I’m not. I didn’t budget for a single coffee or a friend’s birthday gift. When life happened, the whole thing fell apart. The fix: Add a small, $25-$50 ‘Miscellaneous/Oops’ category. It’s the pressure release valve that keeps the whole engine from exploding. A perfect budget that fails is useless; a good enough budget that you stick to is priceless.

Your Step-by-Step Action Plan: The First 90 Days of Freedom

Your first 90-day plan is to save a $1,000 starter emergency fund, list all your debts from smallest to largest, choose the Snowball method, and automate your extra payments toward the smallest debt.

Talk is cheap. Action creates change. Here is your exact plan for the next three months.

Step 1: The Non-Negotiable $1,000 Starter Emergency Fund.

Before you pay an extra dime toward your debt, you must save $1,000 in a separate savings account. This is “life insurance for your debt-free journey”. It’s what prevents a flat tire or an unexpected vet bill from becoming a new credit card balance, which would completely derail your progress and your morale. Selling stuff, working extra hours, eating rice and beans, doing whatever it takes to get this $1,000 saved.

Step 2: The “Ugly Truth” Session.

It’s time to face the monster. Get a complete, honest picture of what you own. Use a tool like the free Debt Payoff Planner app or a simple spreadsheet from a source like Vertex42 to list every single debt, its total balance, minimum payment, and interest rate. Then, go to AnnualCreditReport.com, the only official, federally mandated site and pull your free credit reports from all three bureaus to make sure you haven’t missed anything. This will be uncomfortable, but clarity is the first step toward control.

Step 3: Automate Your Attack.

Willpower is a finite resource. Don’t rely on it. Set up automatic minimum payments on all your debts to go out a day or two after you get paid. This prevents late fees. Then, set up an additional, manual payment for your “shovel” amount to go toward your smallest debt. Pay it the same day you get your paycheck before you have a chance to spend it elsewhere.

Case Study 2: Mark’s $50,000 Payoff in 18 Months

Mark had $50,000 in student loans and credit cards on a $70,000 salary. He felt hopeless. After building his bare-bones budget, he found his “shovel” was $1,200 per month. In his first 90 days, he saved his $1,000 emergency fund. He started the Debt Snowball, attacking a $750 PayPal credit balance. He paid it off in Month 1. The psychological win was massive. He then rolled that payment into the next debt. He became obsessed with watching the balances fall in his Undebt.it app. 18 months later, he was debt-free. The key wasn’t a huge income, but relentless focus and the momentum from those early wins.

The Best Debt & Budgeting Tools for 2026 (A Brutally Honest Review)

The best overall debt payoff app is Debt Payoff Planner for its simplicity, while YNAB is the best for intensive zero-based budgeting. Free options like Unbury.me and Vertex42 spreadsheets are excellent for starting without a cost.

I’ve tested dozens of apps and tools over the years. Most are overly complicated or just trying to sell you something. Here’s what’s worth your time and money. For a simple, motivating visual of your progress, the Debt Payoff Planner app (Free/$2 per month) is my top pick. For an all-in-one life-changing system (if you’re willing to commit), YNAB ($109/year) is unmatched. For a free, no-frills web tool to just run the numbers, Unbury.me is fantastic.

Top Debt Payoff & Budgeting Apps Compared (as of 2026)

| Tool Name | Cost (as of 2026) | Platform | Best For… | My Honest Take (Pro) | The Catch (Con) |

| Debt Payoff Planner | Free / $2 per month | iOS/Android, Web | Visualizing your debt snowball/avalanche progress. | Simple, motivating, and laser-focused on one thing: tracking debt payoff. | Lacks full budgeting features; it’s a tracker, not a complete system. |

| YNAB | $109 per year | iOS/Android, Web | Hands-on, zero-based budgeting for total financial control. | It will fundamentally change your relationship with money. The best system out there. | Steep learning curves and requires consistent, hands-on effort. It’s a commitment. |

| Unbury.me | Free | Web | Quickly comparing Snowball vs. Avalanche without creating an account. | The simplest, fastest way to see your payoff timeline. No sign-up required. | Very basic. Doesn’t save your data or track progress over time. |

| Vertex42 | Free / $9.95 | Excel, Google Sheets | Spreadsheet lovers who want to manage their finances offline. | Highly customizable and powerful if you’re comfortable with spreadsheets. | 100% manual entry. No bank syncing or mobile app. |

| Undebt.it | Free / $12 per year | Web | People who want more payoff methods and integrations (like with YNAB). | The most feature-rich debt planner, with tons of custom strategies. | The free version is limited, and the web interface feels a bit dated. |

| Monarch Money | $99.99 per year | iOS/Android, Web | A modern, all-in-one alternative to Mint for tracking spending and net worth. | Beautiful interface and great for couples. Strong investment tracking. | Budgeting features are less prescriptive than YNAB’s. More of a tracker than a plan. |

| EveryDollar | Free / $79.99 per year | iOS/Android, Web | Simple, zero-based budgeting for fans of Dave Ramsey. | Very easy to use and great for beginners to the zero-based concept. | The free version is manual entry only. Bank syncing requires the paid version. |

Advanced Tactics: How to Negotiate with Creditors (and Win)

To negotiate with creditors, call them directly, explain your situation calmly, leverage your payment history, and ask for a lower interest rate or a fee waiver. Always get any agreement in writing before making payment.

Here’s a secret the credit card companies don’t advertise, almost everything is negotiable. They would rather get paid slowly at a lower interest rate than not get paid at all. You have more power than you think, especially if you have a history of on-time payments.

Before you call, have your account number, your last statement, and your budget handy. Be polite, firm, and persistent. The person on the other end of the phone is just doing their job. Your goal is to make it easy for them to help you.

Actionable Negotiation Scripts

Interest Rate Reduction Script:

“Hello, my name is, and my account number is [Number]. I’ve been a loyal customer for [X] years and have a strong payment history. I’m currently working on an aggressive debt payoff plan and would like to request a reduction in my current APR to help me achieve this. What options are available to me?”

Hardship Plan Script:

“Hello, I’m calling because I’m experiencing a temporary financial hardship due to [brief, honest reasons like a medical issue or reduced hours at work]. I am committed to paying my debt and I’ve created a budget that shows I can afford to pay [$X] per month. I’d like to discuss setting up a temporary hardship payment plan to ensure I can keep my account in good standing while I get back on my feet.”

Remember, debt collectors must follow rules under the Fair Debt Collection Practices Act (FDCPA) and Regulation F. They cannot harass you or lie to you. And be wary of debt settlement companies that charge large upfront fees; they often damage your credit score and fail to deliver on their promises. You can do this yourself for free.

The “Income Shovel”: Creative Ways to Find an Extra $500/Month

To make extra money for debt, go beyond gig work. Consider renting out assets like a spare room on Airbnb or your car on Turo, selling niche skills on Fiverr or Upwork, or selling used clothes and electronics on platforms like Poshmark and Swappa.

The fastest way to accelerate your debt payoff is to increase the size of your “shovel” the extra money you can throw at your debt each month. Driving for Uber or DoorDash is fine, but it saves a lot of time for money. Let’s get more creative.

- Sell Your Skills: Are you great at organizing spreadsheets? Proofreading essays? Designing presentations? List these micro-services on Fiverr or Upwork. You can earn money from your couch without leaving your day job.

- Sell Your Stuff: Use Poshmark for clothes, Facebook Marketplace for furniture, and Swappa for old electronics. A weekend of decluttering can easily become your first snowball payment.

- Rent Your Assets: Use Turo to rent out your car when you’re not using it. Have a spare room? Airbnb. You can turn a liability (car payment) or an unused space into an income stream.

Case Study 3: How a Side Hustle Paid Off a Car Loan

Jenna had a $9,000 car loan she hated. She loved dogs. So, she signed up for Rover to do dog-walking and pet-sitting on weekends. She consistently made an extra $400-$600 a month. Combined with her regular car payment, she paid off the entire loan in just over a year, freeing up $350 in her monthly budget forever. She turned a passion into a debt-destroying machine.

FAQ: Your Toughest Debt Questions, Answered

Q: Is it ever okay to use a balance transfer card or consolidation loan?

A: Yes, but with extreme caution. It’s only a good idea if you can get a significantly lower interest rate AND you have fixed the spending behavior that got you into debt in the first place. Otherwise, you’re just shuffling deck chairs on the Titanic and might end up with more debt when you run up the old cards again. Treat the cause, not just the symptom.

Q: What if my debt is already in collections?

A: First, validate the debt is yours by requesting proof in writing. Debt collectors often have incorrect information. Then, you can negotiate a settlement, often for much less than you owe (they buy debt for pennies on the dollar). Offer a lump-sum payment if possible, and ALWAYS get the settlement agreement in writing before you pay a dime.

Q: Should I stop my 401(k) contributions to pay off debt?

A: This is a controversial topic, but here is my rule: ALWAYS contribute enough to get your full employer match. That’s a 100% return on your money, and you’ll never beat that. You can temporarily pause contributions above the match to attack high-interest debt (anything over 10%). Never, ever stop contributing at the expense of the match to pay off low-interest debt like a mortgage or federal student loans.

Q: I’m married. Is my spouse’s debt my debt?

A: This is a common myth with a complicated answer. Generally, debt you incurred before marriage is legally yours alone, unless your spouse co-signed on the loan. However, debt incurred during the marriage can be considered joint (“marital”) property, especially in community property states. This is less a legal question and more a relationship one. You’re a team, and you need to tackle this together with open and honest communication.

Conclusion: Life After Debt Is Closer Than You Think

Getting out of debt isn’t a math equation you solve. It’s a mountain you climb. It requires a map (your budget), the right gear (your payoff method), and most importantly, the will to take that first, difficult step. We’ve covered the psychology that holds you back, the tactics that propel you forward, and the tools that light the way.

Now, imagine another 2 AM, a year from now. But this time, you’re sleeping soundly. The bills are automated. You have a savings account that’s growing. The monster under the bed is gone. That peace is what we’re fighting for. It’s not just about a zero balance on a statement; it’s about freedom. The freedom to choose, to dream, to live without that crushing weight on your chest.

Your journey doesn’t start tomorrow. It starts right now.

In the comments below, tell me: What is the very first, smallest debt you’re going to attack? Let’s declare it and hold each other accountable. Your first breath of fresh air starts now.

Alex Rodriguez specializes in simplifying investing and financial planning so beginners can feel confident taking their first steps. With a background in finance and a passion for financial literacy, he breaks down topics like index funds, retirement accounts, and long-term wealth-building into plain language and realistic action plans. At Dollar Pioneer, Alex creates guides and tools that help readers understand their options, compare strategies, and build investment habits that support their long-term goals, not just quick wins.