Debt Snowball vs Avalanche and Which is Best for You

It was 2 AM on a Tuesday, and I was staring at a spreadsheet that felt more like a confession. The numbers glowed in the dark, a constellation of my worst financial decisions: $22,000 in credit card debt across three cards, a $16,000 car loan, and the big one $75,000 in student loans that felt like a life sentence. My wife and I were working hard, making decent money, but we had nothing to show for it. We were drowning, and the stress was a constant, low-grade hum in the background of our lives.

That night, I fell down the internet rabbit hole of debt repayment. Every article, every forum, every guru screamed the same two names at me: Debt Snowball and Debt Avalanche. One was supposedly for the emotional, the other for the logical. One was about quick wins, the other about mathematical purity. It felt like a personality test. Are you a feeler or a thinker? Pick a side.

But here’s what nobody tells you: framing the debt snowball vs. debt avalanche debate as a simple choice between math and emotion is fundamentally wrong. It’s a lazy, surface-level take that ignores the deep behavioral science at play and, frankly, insults your intelligence. After a decade in financial technology, building the very tools designed to solve this problem, and after clawing my own way out of that six-figure hole, I can tell you the best method isn’t about picking a team. It’s about understanding your own unique “Debt Fingerprint” and building a strategy that’s as personal as your signature.

In this guide, we’re going to dismantle the old debate. You will discover:

- The unassailable math that shows exactly how much the “feel-good” method can cost you.

- The surprising psychological biases that make the “wrong” choice feel so right.

- Real case studies including my own of people who paid off over $100,000 in debt.

- A contrarian approach called the “Debt Blizzard” that might be the best of both worlds.

- An honest, no-fluff review of the best debt payoff apps for 2026.

By the end of this, you won’t just pick a method. You’ll have a custom-built strategic plan to become debt-free, one that works with your brain, not against it.

What Exactly Are the Debt Snowball and Debt Avalanche Methods?

Before we can break the rules, we should understand them. At their core, both strategies agree on two things: you must make the minimum payment on all your debts, and you must find extra money in your budget to throw at one debt at a time. The disagreement is about the order.

The Debt Avalanche: A Strategy for the Inner Spock

The debt avalanche method is the darling of financial purists and spreadsheet wizards. The logic is cold, hard, and mathematically perfect.

Here’s the process:

- List Your Debts by Interest Rate: You ignore the balances and list every single debt you have, from the highest interest rate (your 2.9% APR credit card) to the lowest (your 4.5% student loan).

- Make Minimum Payments: You continue to pay the minimum required amount on every debt to stay in good standing.

- Attack the Highest Rate: You take every extra dollar you can find in your budget and apply it to the principal of the debt with the highest interest rate.

- Create the Avalanche: Once that top-priority debt is gone, you “avalanche” its entire former payment (the minimum plus all the extra money) onto the debt with the next-highest interest rate. Repeat until you’re free.

The entire premise is to save the most money possible. By targeting the most expensive debt first, you stop that high-interest fire from spreading, which almost always means you pay less in total interest and get out of debt faster.

The Debt Snowball: A Strategy for the Human Being

The debt snowball method, popularized by Dave Ramsey, throws pure math out the window and focuses on something else entirely: momentum.

Here’s the process:

- List Your Debts by Balance: You ignore the interest rates and list all your debts from the smallest balance (that pesky $275 medical bill) to the largest (the giant student loan).

- Make Minimum Payments: Just like the avalanche, you pay the minimum on everything.

- Attack the Smallest Balance: You throw all your extra money at the smallest debt until it’s wiped out.

- Create the Snowball: Once that smallest debt is gone, you take its entire payment and “snowball” it onto the next-smallest debt. Your payment grows with each debt you eliminate, like a snowball rolling downhill.

This method is designed for psychological wins. The goal is to get a quick victory, to feel that jolt of accomplishment from eliminating a debt. That feeling, proponents argue, is the fuel you need to stay in the fight for the long haul.

Let’s Do Math: How Much Does the Debt Snowball Actually Cost You?

This is where the debate usually gets heated. Avalanche proponents will tell you snowballs are a financially irresponsible choice. Snowball fans will say the motivation is worth the price. But what is the price?

Let’s stop talking in hypotheticals and run the numbers on a realistic scenario I see all the time. Let’s call this “The Mixed Bag,” a common debt profile for a household in 2026.

- Store Credit Card: $1,000 balance at 29.9% APR

- Visa Credit Card: $12,000 balance at 17.9% APR

- Car Loan: $15,000 balance at 8.0% APR

- Student Loan: $36,000 balance at 6.0% APR

Let’s assume you’ve worked through your budget maybe using a tool like and found an extra $300 per month to put toward your debt.

Here’s how it plays out:

| Metric | Debt Avalanche (Interest-First) | Debt Snowball (Balance-First) |

| Payoff Order | Store Card -> Visa -> Car -> Student Loan | Store Card -> Visa -> Car -> Student Loan |

| Total Interest Paid | $15,312 | $16,988 |

| Payoff Timeline | 58 Months (4 years, 10 months) | 61 Months (5 years, 1 month) |

| The “Cost of Motivation” | $1,676 more in interest |

(Note: In this specific case, the smallest balance is also the highest interest rate, so the first debt is the same. The difference emerges on the second debt, where Avalanche targets the 17.9% Visa and Snowball targets the $15,000 car loan.)

Seeing it laid out like this changes the conversation. The question is no longer “Which is better?” but “Is the motivational boost of the snowball worth $1,676 and an extra three months of payments to you?”

For some, the answer is an easy “no.” For others, if that $1,676 is the price of sticking with the plan instead of giving up after six months, it’s the best money they’ve ever spent.

Here’s a pattern interrupting for you: math only matters if you finish. If you choose the “perfect” plan on paper but quit because it feels like a soul-crushing slog, you’ve saved nothing. You’ve just delayed the inevitable. The truly optimal plan is the one you see through to the end.

Why Your Brain Is Hardwired to Love the Debt Snowball (Even When It’s “Wrong”)

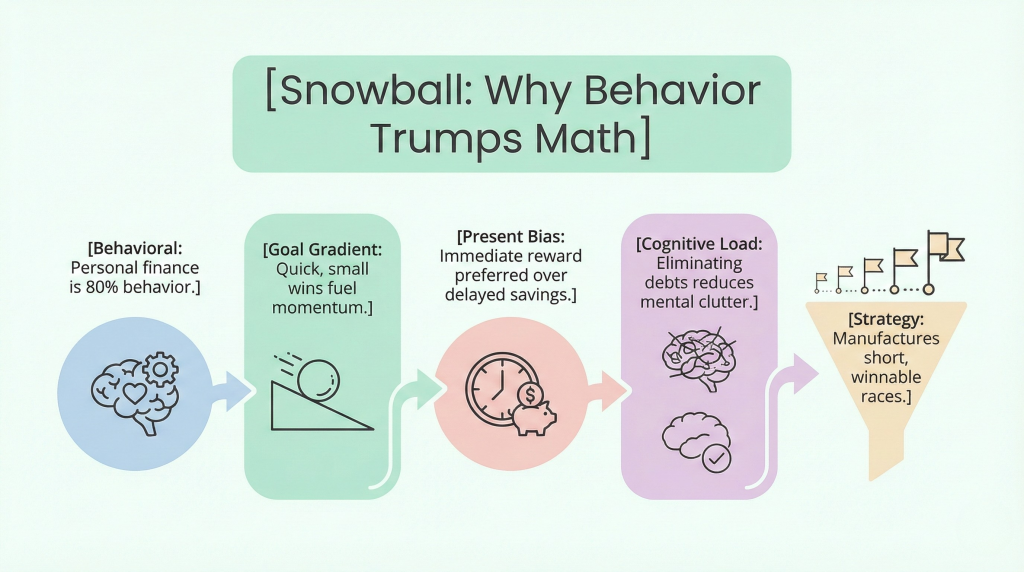

So, if math is so clearly in favor of the avalanche, why do studies and countless success stories show the snowball method is often more effective in the real world? Because personal finance is only 20% head knowledge. The other 80% is behavior.5 Your brain isn’t a calculator; it’s a messy, beautiful, and often irrational machine running on ancient software.

Here’s what’s happening behind the curtain:

- The Goal Gradient Hypothesis: This is a fancy term for a simple truth: the closer you get to a goal, the harder you work to achieve it. Think about how you speed up on the last lap of a race. Paying off a $500 debt feels achievable right now. That finish line is in sight, so you sprint. Paying off a $50,000 loan feels like a distant abstraction, making it hard to maintain intensity. The snowball method manufactures a series of short, winnable races.

- Present Bias: Our brains are wired to prefer a small reward today over a larger reward in the future. The snowball gives you the immediate, tangible reward of a “Debt Paid!” notification. The avalanche offers the delayed, abstract reward of “interest savings” months or years from now. Your brain will almost always choose the immediate dopamine hit.

- Cognitive Load Reduction: Having eight different debts feels like being attacked from eight different directions. Every time you eliminate one, even a small one, you simplify your financial life. You have one less bill to track, one less due date to remember. This reduction in mental clutter and anxiety is a huge, underrated benefit that frees up brainpower to focus on the next target.

My Confession Booth Moment: Why I Chose Snowball

When I was facing my own $113,000 debt mountain, I built the spreadsheet. I ran the numbers. I knew, with absolute certainty, that the avalanche method would save me around $2,000. And I chose the snowball anyway.

Why? Because my smallest debt was a $150 PayPal Credit balance I had used for some gadget I couldn’t even remember. It was a monument to a stupid impulse buy. The thought of obliterating that debt that specific, annoying reminder of my bad habits in the very first month was intoxicating.

I sold some old furniture and clothes online, scraped together $150, and paid it off. The feeling of closing that account, of getting that “Your balance is $0.00” email, was a bigger motivator than any spreadsheet. That tiny win gave me the energy to tackle the next debt, a $3,500 Chase card. And then the next. That initial momentum was worth every penny of the $2,000 in “lost” savings.

Real Stories, Real Results: How People Paid Off 6-Figure Debt

Theory is great, but proof is in the payoff. Let’s look at how these strategies play out for real people.

Case Study #1: Casey and Meygan’s $200,000 “Extreme Snowball”

Casey and Meygan were a married couple who, five years into their marriage, found themselves over $200,000 in debt from student loans, credit cards, and a bad rental property investment. A late-night panic attack followed by a sudden layoff forced them to get serious.

- Their Method: They went all-in on the debt snowball, following Dave Ramsey’s The Total Money Makeover plan.

- The Sacrifices: This wasn’t just about finding an extra $300. They went to extremes. They moved in with a parent for two years, sold their leased car for a 20-year-old beater, stopped eating out entirely, and the husband started officiating weddings on weekends for extra cash.

- The Outcome: In 3 years, 4 months, and 18 days, they paid it all off. They explicitly credit the snowball’s quick wins for keeping them motivated through the intense sacrifices. “Paying off those smaller debts was motivating for us to keep making the sacrifices needed,” they wrote.

The lesson here? The debt repayment method is only one piece of the puzzle. The real magic happens when you pair a motivating strategy with intense, focused changes to your income and expenses.

Case Study #2: The Reddit User’s “Avalanche Burnout”

This is a story I’ve seen play out dozens of times on forums like Reddit. Let’s call him Alex. Alex has $80,000 in debt, with his largest and highest-interest debt being a $45,000 private student loan at 9.5% APR. He’s a logical guy, so he chooses the debt avalanche.

For six months, he lives on rice and beans and throws an extra $800 a month on loan. He’s paid $4,800. But when he logs into his account, the balance has only dropped by about $2,700 because of interest. Meanwhile, his four other smaller credit card bills keep showing up, a constant reminder of how far he should go. He feels like he’s pouring water into a bucket with a hole in it. Defeated, he gives up and goes back to making minimum payments.

The lesson? The avalanche method demands incredible patience and the ability to find motivation in abstract numbers on a spreadsheet. For many, that’s a recipe for burnout.

The Contrarian View: Why You Shouldn’t Choose Either (or What to Do Instead)

Here’s the biggest secret of the debt payoff world: the debt snowball vs. debt avalanche debate is a false dichotomy. You don’t have to choose. The smartest people I know, and the most successful users of our fintech products, don’t pick a side. They create a hybrid.

Meet the “Debt Blizzard”: The Best of Both Worlds

Some call it a hybrid approach or the “Debt Blizzard”. The strategy is simple and brilliant:

- Start with Snowball: Look at your list of debts and identify the one or two smallest balances. Attack them with everything you’ve got. Get those quick, powerful, motivating wins in the first few months.

- Switch to the Avalanche: Once you’ve built momentum and confidence, and freed up some cash flow, pivot your strategy. Re-sort your remaining debts by interest rate and start attacking the most expensive one.

This approach acknowledges a critical truth about the human journey of debt freedom: your needs change over time. At the beginning, your biggest need is motivation. You need to believe you can do it. Later, once you’re in a groove, your biggest need becomes efficiency. You want to save as much money as possible. The Debt Blizzard serves both needs at the right time.

My Expert Take: Create Your “Debt Fingerprint”

I believe we can take this a step further. The future of debt management isn’t a pre-packaged method; it’s true personalization. I call this your “Debt Fingerprint,” a unique profile based on your numbers, your psychology, and your life.

Before you start, ask yourself these three questions:

- The Numbers: What is my interest rate spread? (The difference between your highest and lowest APR). If the spread is huge (e.g., a 25% credit card and a 4% loan), the avalanche has a strong mathematical case. If it’s small (e.g., all your student loans are between 5-7%), the math is a wash, and the snowball’s motivation is more valuable.

- Psychology: What truly bothers you more? Is it the feeling of wasting money on interest every month? Or is it the stress and clutter of having multiple bills to pay? Be honest. Your answer points to your natural inclination. If you hate waste, you’re an “Optimizer” (Avalanche). If you hate clutter, you’re a “Simplifier” (Snowball).

- The “Nuisance” Factor: Is there one specific debt that just drives you crazy? Maybe it’s a loan from a family member, or that stupid PayPal credit from my story. Sometimes, the best first target is the one that provides the most emotional relief, regardless of its size or interest rate.

Answering these questions gives you a personalized roadmap that’s far more powerful than picking a generic, one-size-fits-all plan.

The Best Debt Payoff Apps in 2026, Honestly Reviewed

You don’t have to manage this journey with a pen and paper (though you can!). The right technology can be a powerful co-pilot. I’ve tested, analyzed, and even helped build dozens of these tools. Here are my honest assessments of the best options available today.

- For the Hands-On Budgeter: YNAB (You Need a Budget)

- What it is: YNAB is a digital version of the envelope budgeting system. It’s a proactive philosophy that forces you to give every single dollar a “job.” It has a fantastic loan payoff simulator that lets you model how extra payments affect your debt-free date.

- Honest Assessment: YNAB has a steep learning curve and requires commitment. It’s not a passive tracker; it’s an active management tool. But for people who stick with it, life is changing. It’s pricey at $14.99/month, but it’s the best tool for fundamentally changing your relationship with money, which is the root cause of debt.

- Best for: People who want to fix the spending habits that got them into debt in the first place.

- For the Debt-Focused Planner: Undebt.it

- What it is: This is a pure debt-crushing machine. It’s a web-based tool that supports over eight payoff methods, including Snowball, Avalanche, and custom plans. It provides detailed charts and timelines to track your progress.

- Honest Assessment: The free version is incredibly powerful. The premium version ($12/year) unlocks even more customization. Its biggest weakness is that it’s not a budgeting app; it assumes you’ve already figured out how much extra you can pay. But for pure debt modeling, it’s unbeatable.

- Best for: Data nerds who want to compare different payoff scenarios and track their journey with precision.

- For Finding Extra Money: Rocket Money

- What it is: Rocket Money’s genius is in finding money you didn’t know you had. It identifies and helps you cancel unwanted subscriptions, and its team will even negotiate lowering your monthly bills (like cable or cell phone) on your behalf.

- Honest Assessment: This isn’t a debt strategy app, but it’s a fantastic tool for funding your strategy. Finding an extra $50-$100 a month by canceling unused services or lowering a bill can be the fuel for your snowball or avalanche. The free version is great for tracking; the premium features are where the real savings happen.

- Best for: Anyone who feels their budget is already stretched thin and needs help finding more cash to accelerate their payments.

- For the “Set It and Forget It” Saver: Qapital

- What it is: Qapital automates your savings for specific goals. You can set rules like “round up my purchases to the nearest dollar and save the change” or “save $10 every Friday.” You can create a “Debt Payoff” goal and let the app slowly and painlessly build up a fund for extra payments.18

- Honest Assessment: This is a brilliant tool for people who struggle with the discipline of manually setting money aside. It makes saving for your extra payments effortless. It’s not a full debt management solution, but it’s a powerful way to automate the “funding” part of your plan.

- Best for: People who want to save for extra debt payments without feeling the pinch.

Your Final Action Plan: Which Method Wins?

After all the math, the psychology, and the real-world stories, what’s the verdict in the debt snowball vs. debt avalanche showdown?

Here’s my final, unfiltered opinion, born from a decade of professional and personal experience:

The best method is the Debt Blizzard, guided by your personal Debt Fingerprint.

Start with the quick wins of the Debt Snowball. Get that addictive hit of motivation. Prove yourselves that you can do this. Then, once you have momentum, pivot to the mathematical efficiency of the Debt Avalanche to save the most money in the long run.

Don’t let anyone tell you that you should choose between being smart with your money and being smart about your motivation. You can, and should, do both. The journey out of debt is a marathon, not a sprint. It requires a strategy that can adapt, that honors both the numbers on the page and the human spirit required to see it through.

You’ve read this far, which tells me you’re ready. You’re ready to stop feeling overwhelmed and start taking control. So, my question for you is this:

What is the first small debt you are going to destroy to start your snowball rolling?

Let me know in the comments below. Let’s get this done.

Frequently Asked Questions (FAQ)

1. Is the debt snowball method ever a bad idea?

Yes, it can be a bad idea if you have a debt with a dangerously high interest rate (like a payday loan at 400% APR) that is not your smallest balance. In such extreme cases, interest is accumulating so fast that it can outpace your payments on smaller debts. This is a rare situation where you should prioritize the high-interest debt first, even if it breaks the snowball rule. For most typical consumer debt, however, the snowball is a viable strategy.

2. Does paying off debt hurt your credit score?

Initially, you might see a small, temporary dip in your credit score when you pay off a loan and close the account, especially if it’s one of your older accounts. This is because “age of credit history” is a factor in your score. However, in the medium too long term, paying off debt is overwhelmingly positive for your credit. It lowers your credit utilization ratio (how much debt you have vs. your credit limit), which is a major factor in your score.

3. Should I pause my debt payoff plan to save for retirement?

This is a controversial topic. Dave Ramsey and proponents of the snowball method advise pausing all retirement investing (even a 401k match) to focus 100% of your energy on debt. The mathematical argument is that a guaranteed 401k match is a 100% return you shouldn’t pass up. My nuanced take: at the very least, contribute enough to get your full employer match. It’s free money. Beyond that, it depends on your debt’s interest rates. If you’re paying 25% on a credit card, that’s a guaranteed 25% “return” when you pay it off, which beats the market. If your debt is a 4% student loan, investing might make more sense.

4. What if I have an emergency while paying off debt?

This is why the first step in any good financial plan (including Dave Ramsey’s) is to save a small, starter emergency fund of around $1,000 before you start aggressively paying off debt.23 If a true emergency happens (job loss, medical issue), you should pause your extra debt payments (continue making minimums), use your emergency fund, and pile up cash until the crisis passes.

5. Can I use a debt consolidation loan instead of these methods?

You can but be careful. A debt consolidation loan rolls multiple debts into a single new loan, ideally at a lower interest rate. This can be a great tool if you have good credit and can secure a significantly lower rate. It simplifies your payments and saves you money. However, it doesn’t fix the underlying behavior. Many people consolidate their credit cards, feel relieved, and then run the cards right back up again, ending up in twice the trouble. If you consolidate, you must commit to not creating new debt.

Alex Rodriguez specializes in simplifying investing and financial planning so beginners can feel confident taking their first steps. With a background in finance and a passion for financial literacy, he breaks down topics like index funds, retirement accounts, and long-term wealth-building into plain language and realistic action plans. At Dollar Pioneer, Alex creates guides and tools that help readers understand their options, compare strategies, and build investment habits that support their long-term goals, not just quick wins.